MARKETS

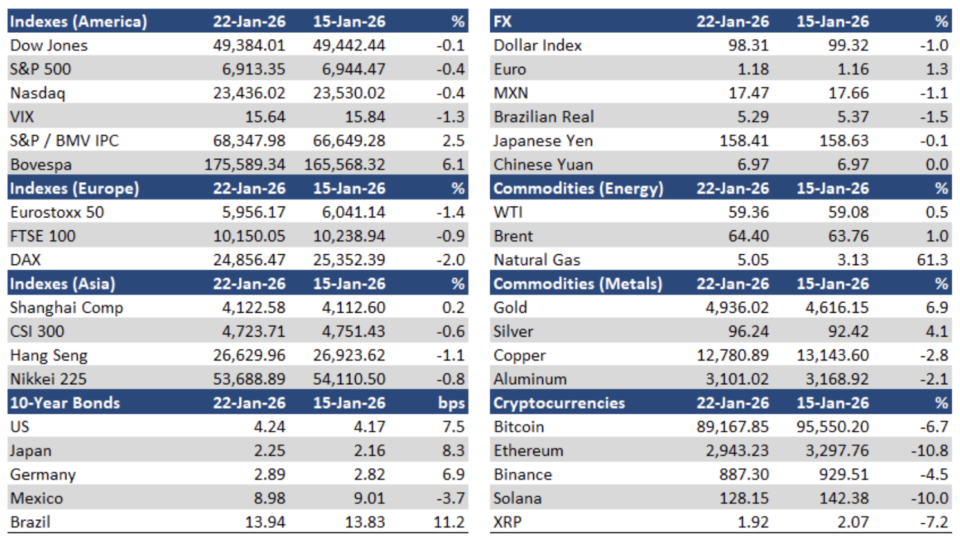

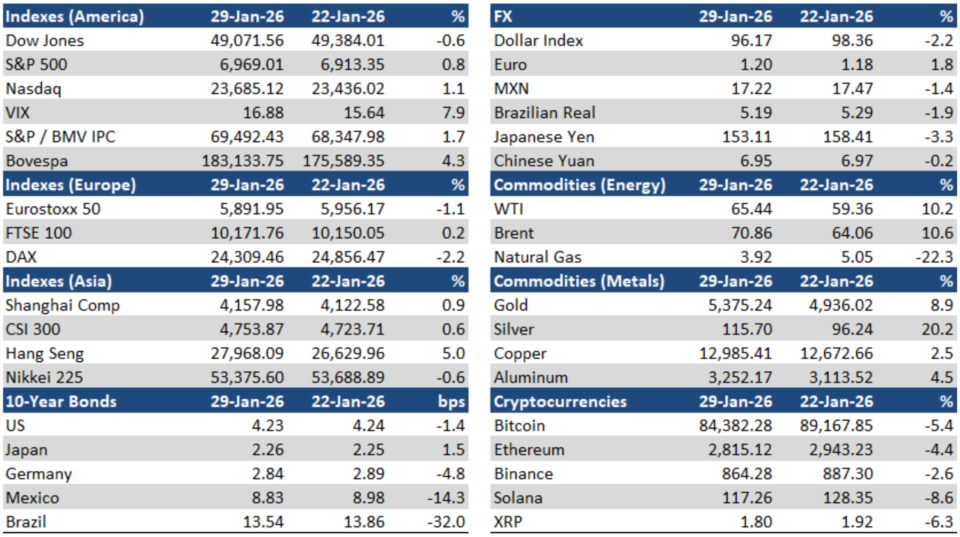

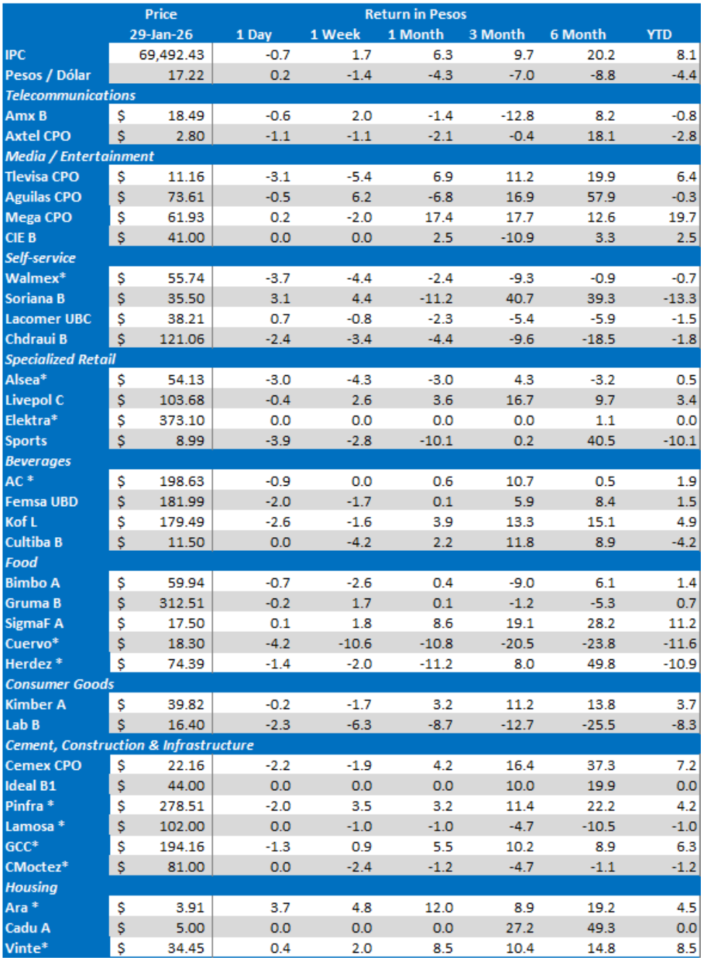

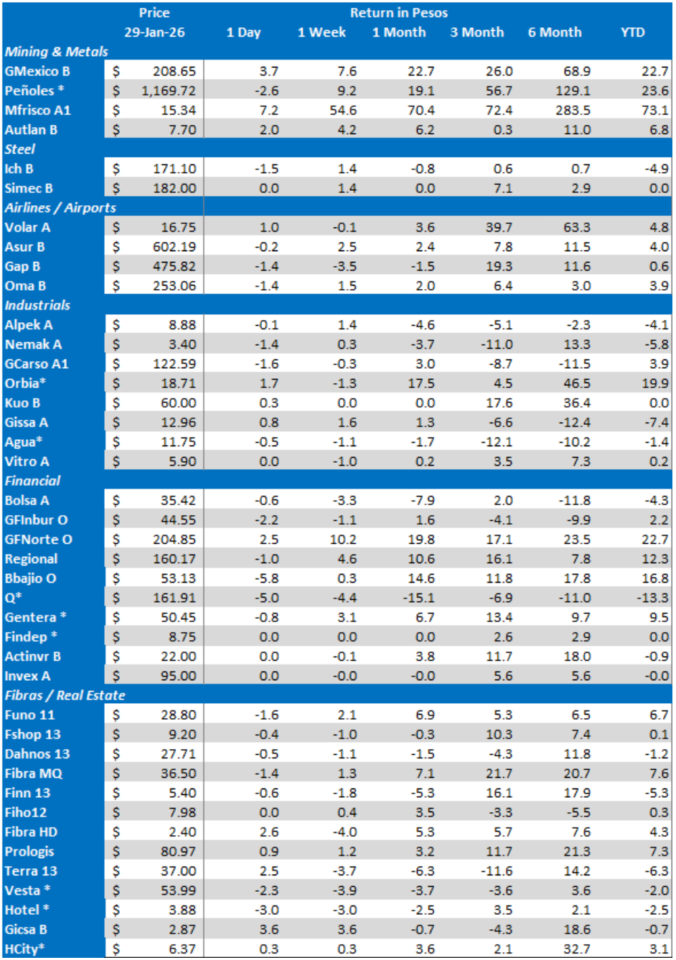

The S&P / BMV IPC was up another 1.7% after setting a new intraday historically high. The index benefited from the rally in GFNorte’s, Peñoles and GMexico’s shares, as well as global risk appetite for emerging markets. Meanwhile, the Mexican peso appreciated 1.4% to close at MXN$17.22/USD; the yield of the 10-year M-Bono was down 14 bps to 8.83%.

The S&P / BMV IPC’s top gainers were: GFNORTE O (+10.2%), PEÑOLES * (+9.2%), and GMEXICO B (+7.6%). On the other hand, the main losers were: CUERVO * (-10.6%), LAB B (-6.3%) and TLEVISA CPO (-5.4%).

LISTED COMPANIES

Grupo México reported strong 4Q25 results, ahead of expectations. Total revenues rose 34% YoY, driven mainly by a 43% increase in mining revenues fueled by favorable metal prices (copper +22%, gold +56% and silver +74%) and higher volumes. Copper production expanded 1.9% YoY due to gains at Caridad, Toquepala, Cuajone, IMMSA and Asarco. Transportation revenues grew 14% YoY supported by higher carloads, longer routes and improved automotive and agricultural demand. Consolidated EBITDA grew 51% YoY, reflecting operating leverage in mining and rail, while the EBITDA margin widened to 55.7%, from 49.5%, on lower cash costs and a richer byproduct mix. Net profit climbed 43% YoY, aided by stronger operating income and cost discipline. The company expects a US$473 million capex in 2026. GMexico is in talks with the Mexican government to reactivate US$10.2 billion in investments.

GFNorte delivered a solid 4Q25, with total portfolio +8% YoY, driven by consumer volumes plus a sharp acceleration in government lending and sustained corporate/commercial momentum. NPL ratio rose 50bps YoY to 1.4%, while CoR normalized to 1.4% in the quarter. Total deposits increased 10% YoY, supported by year-end seasonality and commercial traction. Digital transactions showed a mixed pattern, with mobile monetary transactions +27% YoY and POS transactions down 13% YoY. Net interest income increased 8% YoY, driven by loan growth and lower funding costs that offset reference-rate cuts. NIM expanded 16 bps YoY to 6.6%, reflecting balance-sheet optimization and funding mix discipline, albeit with some dilution from faster government-loan growth. Non-interest income surged 106% YoY, supported by resilient banking fees, stronger market-related results, and an accounting reclassification within insurance claims/provisions. Provisions declined 9% YoY, consistent with a normalization versus 3Q25. Expenses rose only 3% YoY, while the efficiency ratio improved 320 bps YoY to 37.9%. Net profit increased 16% YoY, supported by stronger NII and lower provisioning, and ROE expanded 260 bps YoY to 24.2%. The 2026 guidance includes a 8-11% loan growth, NIM between 6.2-6.5% and net income between MXN$62.0-64.0 billion.

Quálitas posted 4Q25 net losses due to a non-recurring item related to the new income law. Written premiums up +6.4% YoY, supported by financial institutions (+29.4% YoY) and foreign subsidiaries (+21.1% YoY), which more than offset declines in individual (-0.2% YoY) and fleets (-7.2% YoY) amid competitive tariff pressure. Earned premiums rose +8.5% YoY, with reserve constitution broadly stable versus 4Q24, while insured units closed 2025 at ~6.1 million (+335k vs 2024). Profitability deteriorated as the acquisition ratio increased to 22.0% (+77 bps) and the loss ratio climbed to 77.0% (+1,164bp YoY), which led to a combined ratio of 102.6% (+1,249bp YoY). Management attributed the step-up largely to a non-recurring VAT impact linked to the 2026 income law. The combined ratio stood at 89.3%, stripping out the one-off VAT impact. Comprehensive financial income declined -21.3% YoY (ROI 8.1% vs 11.5%), reflecting lower investment income, and net profit swung to a MXN$190 million net loss with a 20.2% ROE due to the same VAT-related distortion. Excluding VAT, the company would have reported a MXN$1.5 billion net profit with a 26.9% ROE. For 2026 guidance, the company expects written premium growth in the high single-digit to low double-digit range, an average premium increase roughly in line with inflation, a loss ratio within or slightly above 62%–65% as the VAT impact absorption progresses, acquisition and operating ratios within historical ranges, and a combined ratio at the upper end of 92%–94% (or slightly above), while financial income stays broadly flat YoY under its fixed-income duration strategy.

Regional posted 4Q25 results, falling short of the annual guidance. The total loan portfolio was up 8% YoY driven by commercial lending expansion while the NPL ratio increased only 1 bps to 1.3% reflecting stable asset quality. Core deposits rose 13% supported by time and demand deposit growth, and digital transactions reached 126.5 million reflecting continued client migration to electronic channels. The financial margin increased 7% YoY driven by loan growth and lower funding costs, but NIM declined 32 bps YoY to 6.3% due to asset mix effects and lower yields despite a reduced cost of funds. Provisions grew 6% YoY, while the adjusted net interest margin advanced by 7% YoY supported by higher earning assets. Net fees and commission were 12.0% higher. Non-interest expenses rose 17% YoY driven by personnel and administrative costs, leading to an efficiency ratio of 42.2% in the current quarter. Net income grew 7% YoY due to higher adjusted financial margin and fee income, and ROE reached 19.1%. Annual net profits grew 2%, below the company’s guidance of 5-10%. The 2026 guidance includes a 5.-10% loan growth with a NPL ratio below 1.8%, +5-10% in deposits, and +5-10% in net income with a dividend payment in line with that of the previous years.

BanBajío reported mixed 4Q25 results, exceeding the net profit guidance for the year. The loan portfolio was up 4.6% YoY (business +5.2%, government +12.1%, consumer +11.4%; financial institutions -11.4% and mortgages -15.4% offset) while the NPL ratio remained virtually unchanged at 1.49%. Deposits grew 10.5% YoY, supported by the funding mix across demand and time deposits. The financial margin fell 7.0% YoY as the reduction in average asset yields was partly cushioned by higher average earning assets, and NIM tightened 100 bps to 5.8%. Provisions declined 15.3% YoY (lower quarterly ECL charge and higher recoveries), and adjusted financial margin slipped 6.0% YoY. Non-interest income grew 11.0% due to higher fees and commissions. Non-interest expenses increased 5.8% YoY, while the efficiency ratio worsened 445 bps to 43.5%. Net profit decreased 15.1% YoY, with ROE at 19.4%, from 24.5%, as margin compression outweighed fee traction and a lighter risk-cost print. The company met its 2025 guidance. For 2026, BanBajío expects: loan growth of 8-10%, NPL ratio below 1.7%, deposits growth +10-11%, NIM 5.5-5.5%, fees + trading income +13+15%, expenses +7-9%, efficient ratio 43-45%, net income MXN$8.25-9.0 billion, ROAE 16.5%-18.0%.

GCC posted solid 4Q25 results, with net sales up 7.3% YoY driven by higher concrete and cement volumes in the US and increased cement volumes in Mexico, as well as higher concrete prices in both countries. These gains were partially offset by decreased concrete volumes in Mexico and lower cement prices in the US and Mexico. EBITDA rose 17.3% YoY supported by operating leverage, cost discipline and a favorable mix, lifting the EBITDA margin by 340 bps to 39.6%, while net income increased 5.6% YoY reflecting higher operating profit despite lower financial income and higher taxes. For 2026, management guided to mid-single digit EBITDA growth, FCF conversion above 60%, total CapEx of US$270 million focused on growth, negative net debt to EBITDA, US cement volumes with a high-single digit increase offset by a high-single digit concrete decline, flat US cement prices, and low-single digit increases in Mexico cement volumes and prices. The company acknowledged that the expansion of its plant in Odessa, Texas, will result in a smaller increase in capacity than previously anticipated, due to changing market conditions in recent years.

Cox ABG Group announced it has secured a US$2.65 billion syndicated loan with Citi, Goldman Sachs, Barclays, Deutsche Bank, Santander, BBVA y Bank of Nova Scotia for the acquisition of Iberdrola’s assets in Mexico. The Spanish company has also obtained the required regulatory approvals from the National Energy Commission and the National Antitrust Commission.

Gruma avoided the sale of 5 plants. The company announced the successful conclusion of an antitrust administrative proceeding in Mexico related to the distribution and commercialization of corn and corn flour products, after an investigation that began in November 2022. The National Antitrust Commission accepted the pro-competition alternative measures proposed by Gruma, which ensure that industrial tortilla makers can freely choose their corn flour supplier and that certain supply agreements are amended to remove exclusivity or minimum purchase commitments, without requiring the divestiture of assets that had been initially proposed. Gruma has between 90 and 180 days to implement such measures.

Grupo Aeroportuario del Sureste’s shareholders approved the previously announced acquisition of Companhia de Participações em Concessões for US$936 million (with an enterprise value of US$2.57 billion) and the assumption of debt to carry out such transaction. CPC owns equity interests in 20 airports with concessions in Brazil, Ecuador, Costa Rica and Curaçao.

Sitios Latinoamérica will propose a MXN$5.0 billion capital subscription at its February 10th Ordinary Shareholder’s Meeting.

Grupo Bimbo is planning to redeem 80 million BIMBO 16 notes on February 10th, 2026. The calculation of the early redemption price will be performed by the Common Representative based on the information provided by the Issuer at least two business days prior to the scheduled date, in accordance with the provisions of the indenture governing the Notes.

On January 28, CMR initiated a transition process for the roles of CEO and Executive Chairman, which will be conducted and supervised by the Board of Directors. After 16 years in CMR, Joaquín Vargas Mier y Terán has decided to conclude his tenure as the company’s CEO and Executive Chairman, while remaining a member of CMR’s Board of Directors.

Peña Verde will buyback up to 52,921,283 of its own shares over the course of this year at an average price of MXN$8.50/share. The repurchases will be executed through several transactions, each representing less than 3% of the company’s share capital and separated by 20 business days.

OTHER COMPANIES

Pemex suspended an oil shipment to Cuba which was originally scheduled for this month. President Claudia Sheinbaum clarified that oil shipments to Cuba are not suspended and are being carried out through two channels: Pemex commercial contracts and humanitarian aid. On the other hand, Pemex reported that oil production declined 7.1% to 1.635 mbpd in 2025, the lowest level since 1980.

CFE issued US$1.5 billion bonds in international debt markets which included: i) US$1.0 billion in an 8-year bullet note with an indicative interest rate of 6.04%; and, ii) US$500 million in a 25-year amortizing note with an interest rate of 6.50%. The company will use proceeds to refinance existing indebtedness and to finance investment projects, respectively, with the securities expected to receive investment-grade ratings from major agencies.

Revolut officially launched operations in Mexico on January 27, setting a target of two million users in its first year and announcing plans to invest an additional US$100 million, on top of the roughly US$100 million already deployed, according to Miguel Guerra, Mexico CEO. A core pillar of its strategy is commission-free remittances between Revolut users in Mexico and the United States, while the company gradually expands its product offering toward full traditional banking services, including payroll portability, auto and mortgage loans, and SME financial services starting in 2027.

Mercado Libre opened a new cross-dock center in the municipality of Cuautitlán Izcalli, State of Mexico, as part of its growth and logistics consolidation strategy in Mexico.

Ticketmaster faces a Profeco investigation due to alleged irregularities on the sale of BTS tickets, with penalties against the company potentially reaching up to MXN$4.0 million. Ticketmaster later stated that ticket sales for BTS recorded unprecedented demand, with 2.1 million users registering to purchase some of the 136,400 tickets available for the three concerts, and a peak of 1.1 million people queued in the so-called “virtual line.” Meanwhile, President Claudia Sheinbaum made a “diplomatic request” to South Korea’s President to increase the number of BTS concerts in Mexico.

Viva Aerobus announced an expansion of its codeshare agreement with Iberia to more than 40 destinations in Europe and selected destinations in the Middle East, including Doha and Tel Aviv. The agreement also includes a new direct Madrid–Monterrey route operating three times per week starting June 2nd, as well as expanded interline connectivity from Monterrey to 32 additional domestic destinations in Mexico, complementing Iberia’s three daily Mexico City–Madrid flights.

Desarrollos Eólicos Mexicanos de Oaxaca 1, S.A.P.I. defaulted on the interests and capital payments of its DMXI 15 domestic bonds which were due last January 26th, due to lack of liquidity resulting largely from problems in the operation of its assets.

Colombian proptech firm TuHabi announced the acquisition of real estate accelerator Pulppo as part of a strategy to accelerate the development of a more efficient, secure, and professional real estate ecosystem in Mexico. Pulppo works with real estate agencies and advisors in Mexico and other markets across the region through a network of 100 agencies, 800 brokers, and a technology platform designed to operate and scale the real estate business.

Sofipo Finsus expects to obtain a full banking license this year after growing its customer base by 64% and its loan portfolio to SME’s by 77% in 2025.

ECONOMIC

USTR Jamieson Greer agreed with Economy Secretary Marcelo Ebrard to begin formal discussions on possible structural and strategic reforms in the context of the first USMCA Joint Review, including stronger rules of origin for key industrial goods, enhanced collaboration on critical minerals, and increased external trade policy alignment to defend workers and producers in the US and Mexico and to combat the relentless dumping of manufactured goods in the region.

The IGAE fell 0.2% YoY (seasonally adjusted) in real terms in November, which was below the 0.2% expected increase of the latest INEGI survey and the 1.0% MoM rise of the previous month. Primary activities declined 7.0% and tertiary activities 0.4%, while secondary activities advanced 0.6%. The IGAE fell 0.1% YoY (originally data) in November, below the 2.3% expected growth according to the INEGI survey. Secondary activities were down 0.8%, which was partially offset by a 1.3% increase in primary activities and a 0.2% growth in tertiary activities.

Construction activity gained traction after rising 1.7% MoM in November, which was the best performance since June 2024, according to INEGI. However, construction activity fell 8.0% YoY, accumulating 19 months in negative territory.

Unemployment fell to 2.39% in December, the lowest level since 2005, according to INEGI. This figure compares favorably to 2.66% in November 2025 and 2.43% in December 2024.

The trade balance registered a US$2.43 billion surplus in December, INEGI reported. Total exports grew 17.2% YoY (oil -32.9%, non-oil +19.5%) to US$60.7 billion while total imports advanced 16.7% (oil -0.7%, non-oil +18.2%) to US$58.2 billion. In 2025, the trade balance recorded a US$770.9 million surplus, the first since 2020, as exports increased 7.6% to a record level of US$664.8 billion, while imports were up 4.4% to US$664.1 billion.

Banco de México’s Governing Board stated in the 2026 Monetary Program that it will assess the appropriate timing for making additional adjustments to the policy interest rate this year, in order to observe the evolution of certain indicators within the inflation outlook.

President Claudia Sheinbaum met with members of the Mexican Banking Association (ABM). She said that the Mexico Plan seeks to boost growth through increased financing, accelerated digitalization, and the strengthening of financial inclusion, with an emphasis on tools such as digital identity and CoDi to expand access to financial services.

CETES auction: 28-day CETES -5 bps to 6.95%; 91-day CETES flat at 7.10%; 175-day CETES -12 bps to 7.14% and 693-day CETES -7 bps to 7.82%.

Download PDF: Mexican Market Chatter January 22nd – 29th