MARKETS

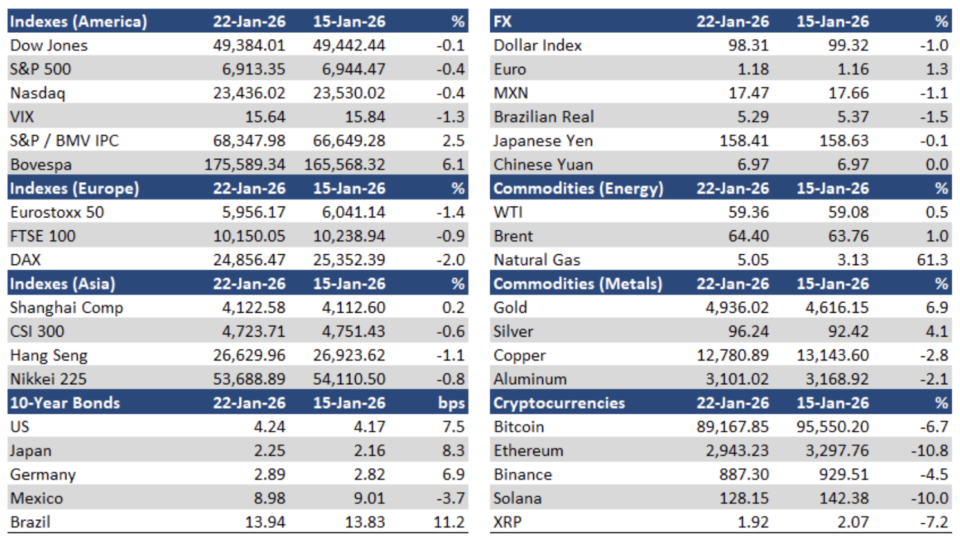

The S&P / BMV IPC rallied another 2.5% over the last week, closing at new historical highs, fueled by a firm risk-on tone in global financial markets, with US indices trading near their highs. Meanwhile, the Mexican peso appreciated 1.1% to close at MXN$17.47/USD; the yield of the 10-year M-Bono was down 3 bps to 8.98%.

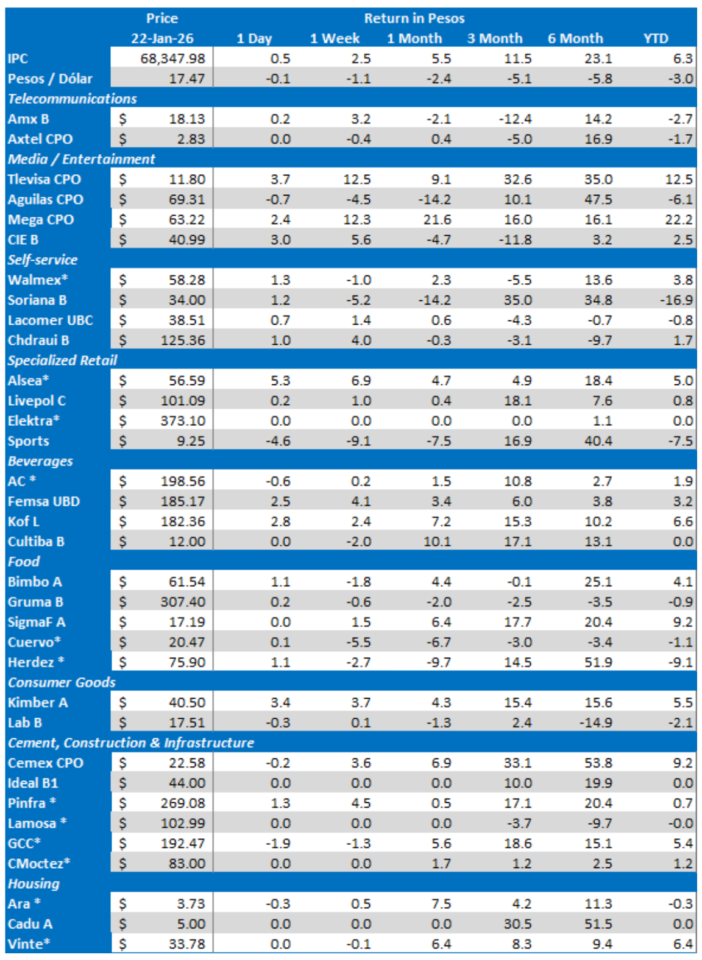

The S&P / BMV IPC’s top gainers were: BBAJIO O (+13.2%), TLEVISA CPO (+12.5%), and GAP B (+8.4%). On the other hand, the main losers were: CUERVO * (-5.5%), Q* (-3.3%) and BIMBO A (-1.8%).

LISTED COMPANIES

JPMorgan Chase disclosed it has acquired a 5.5% equity stake (140.9 million CPO’s) in Grupo Televisa, likely on behalf of third parties. This equity stake currently has a market value of around US$86 million. BlackRock also disclosed it has increased its equity stake in Grupo Televisa by 0.45% to 5.3% (134.4 million CPO’s), likely via its ETFs, thus becoming a relevant shareholder.

Kimberly Clark de Mexico reported positive 4Q25 results with higher-than-expected EBITDA and net profits. Quarterly results reflected continued operating momentum, with total revenues up 2% YoY, supported by a 5% increase in consumer products that offset declines in Away from Home and export volumes. Gross profit advanced 5% YoY and gross margin expanded to 40.4%, driven by favorable input costs, a lower average FX rate, and MXN$500 million in quarterly cost savings. EBITDA grew 6% YoY, with the EBITDA margin reaching 26.4% at the high end of the long-term target range, supported by cost discipline and operating leverage. Net income rose 23% YoY, reflecting stronger operating performance despite higher financing costs and an adverse FX comparison.

Grupo Carso entered into a binding agreement with Lukoil International Upstream Holding B.V. and Lukoil International Holding GMBH, for the acquisition of 100% of its subsidiary Fieldwood Mexico B.V., which in turn directly and indirectly owns 100% of the share capital of (i) Fieldwood Energy de México, S. de R.L. de C.V., and (ii) Fieldwood Energy E&P México, S. de R.L. de C.V. (“Fieldwood México”). Fieldwood México is the “operating” entity and holder of a 50% interest in the Ichalkil & Pokoch fields (“Contract Area 4”), a contract area located off the coast of Campeche. The purchase price for 100% of the company’s share capital is US$270 million, in addition to assuming the obligation to pay off the company’s debt of US$330 million to Lukoil, the seller. These figures and payment terms are subject to closing adjustments in accordance with the terms of the contract.

Industrias Peñoles’ subsidiary Fresnillo plc has successfully completed the previously announced acquisition of Probe Gold Inc. after receiving all required approvals from Probe’s shareholders, the Canadian court, and regulators. Fresnillo plc has paid approximately CAD$770 million (around US$555 million) using available cash.

Nemak’s Board of Directors has appointed Hervé Boyer as its new CEO effective April 1st, 2026. He will replace Armando Taméz, after the latter’s 42-year career at Nemak including 13 years as CEO.

Esentia Energy has begun the construction of the Aguascalientes Compression Station, as part of its expansion plans in Mexico, according to local newswires. The project is part of the first of three expansion phases, which will require a total investment of US$680 million. The project will allow the company to increase its gas transport capacity along the Villa de Reyes-Aguascalientes-Guadalajara (VAG) system, starting in early 2027.

Betterware de México has agreed to acquire Tupperware’s operating assets in Latin America, mainly in Mexico and Brazil, for US$250 million. It also acquired a perpetual, royalty-free, and exclusive license to the Tupperware brand in Latin America. The transaction will include a US$215 million cash payment, to be financed with debt, plus an additional US$35 million in Betterware de México shares. The implied acquisition multiples are 3.1x EV/EBITDA 2025E and 5.6x P/E 2025E, contributing an estimated EPS of US$0.58 and US$81 million in annual EBITDA, representing an immediate earnings accretion of approximately 40% per share. The acquisition will be financed with debt which will increase the 2025E net debt to EBITDA ratio from 1.6x to 1.9x and is not expected to impact Betterware’s current dividend policy.

Alsea announced the full prepayment of US$500 million and EUR300 million in Senior Unsecured Notes. The company financed itself with new sustainability-linked bank facilities which included a MXN$10.5 billion club deal in Mexico with a 5-year bullet maturity and a floating rate of TIIE + 145 bps and a syndicated loan of up to EUR 550 million in Europe, with a 5-year amortizing maturity and a floating interest rate of Euribor + 210 bps. The transaction is expected to lower annual interest expense by approximately US$25 million by 2026, extend average debt maturity beyond four years, reduce FX exposure, and reinforce the company’s ESG commitments.

Grupo Aeroportuario del Pacífico refinanced its US$95.5 million bank loan with Scotiabank Inverlat though a new financing from The Bank of Nova Scotia maturing on January 19th, 2027, with an option for early repayment. The loan will accrue interest payable monthly at a variable rate equivalent to SOFR 1M plus 50 basis points, with no additional fees.

Fibra Macquarie México closed a US$50.0 million sustainability-linked unsecured credit facility. The financing provides additional liquidity and funding capacity to enhance FIBRA Macquarie’s financial position, while extending debt maturities. As a result of the transaction, FIBRA Macquarie’s funding cost remains efficient at approximately 5.5% per annum while increasing available liquidity to US$615.0 million through committed and uncommitted credit facilities.

Telecommunications sector. 2.15 million lines have been registered under the mandatory registration process, according to José Antonio Merino, head of the Digital and Telecommunications Transformation Agency.

GMexico Transportes announced it cancelled the listing of its shares in the Mexican Bolsa last January 15th after receiving approval from the CNBV.

OTHER COMPANIES

General Motors has terminated 1,900 employees of its Ramos Arizpe plant, related to reduction in US demand for electric vehicles following cuts in subsidies and tariffs on Mexican car exports to the US. The company transferred some production to the US, likely to mitigate tariffs.

The FinTech bank Ualá, which has struggled to gain traction in Mexico versus other credit card –focused FinTechs such as Nu, Plata, Klar, Stori – announced the integration of its credit cards into Apple Pay in Mexico as part of its strategy to boost adoption of contactless payments.

ECONOMIC

Mexico’s Economy Shows a Modest Upside Surprise to End the Year

Mexico’s economy ended the year on firmer footing than many had expected, offering a modest upside surprise amid a still-cautious backdrop. According to a preliminary estimate released by Mexico’s national statistics agency, INEGI, economic activity likely expanded 2.3% year-on-year in December. On a monthly basis, activity was estimated to have increased 0.2% compared with November, pointing to some momentum at the close of the year. Mexico’s industrial production MoM rose by 0.6% in November and declined by just 0.1% YOY (vs. -0.5% in October), driven by a rebound in construction, the best performance in a while. Analysts may end up upgrading full year 2025 GDP growth a little if future data releases for 4Q25 coincide with these numbers.

The Mexican Government has acquired hedges to guarantee 2026 oil export revenues, according to Hacienda Minister Edgar Amador. He mentioned that the price is in line with the projections of the 2026 Economic Package. Hacienda also successfully completed its first refinancing operation in the local market amounting to MXN$235.55 billion. Additionally, it carried out a MXN$10.408 billion syndicated placement of new 30-year Udibonos with a 4% real interest rate. According to Hacienda, both transactions optimized the maturity profile of peso-denominated debt at fixed nominal and real rates, strengthening the structure of the government portfolio, and improving the liquidity conditions of the local market by incorporating a new long-term benchmark.

Headline inflation rose 0.31% in the first half of January 2026, which was below the Citi Mexico Expectations Survey 0.40% consensus projection. Core inflation increased 0.43% in the same period, also below the 0.47% consensus forecast, driven mainly by higher food, beverages and tobacco prices. The bi-weekly non-core inflation rate declined 0.12%, primarily reflecting lower prices for agricultural products and energy categories. On an annual basis, headline inflation stood at 3.77% and core inflation at 4.47%.

Service sector’s revenues increased 0.7% MoM (seasonally adjusted) in November, the best performance in the last six months, according to INEGI. As a result, service sector revenues rose 1.4% YoY based on original data.

Retail sales were up 1.0% MoM (seasonally adjusted) in November, INEGI reported. Retail sales advanced 4.4% YoY (original data).

Manufacturing production grew 1.0% MoM (seasonally adjusted) in November, INEGI reported. However, manufacturing production advanced 0.1% YoY based on original figures.

Consensus expects Banco de Mexico to cut its reference interest rate by 25 bps at the May meeting, unchanged versus the previous survey, according to the January 20th, Citi Mexico Expectations Survey. The median policy rate forecast remained unchanged at 6.50% for YE26 and YE27. GDP growth expectations remained stable, with the median forecast for 2025 at 0.4%, and for 2026 at 1.3%. Headline inflation expectations for YE26 remained at 4.0%, while core inflation expectations for the same year also hold at 4.0%; for YE27, both headline and core inflation expectations stand at 3.7%. Peso expectations improved, with consensus now projecting an FX rate of 18.75 by YE26, from 19.00 previously, and 19.07 by YE27, from 19.50 in the prior survey.

Foreign investment in Mexican equities increased by US$320 million in December, Banco de México reported. However, foreign investment outflows amounted to US$4.7 billion throughout 2025, which was the third year in a row with a negative figure.

Mexico’s fiscal revenues increased 4.8% YoY in real terms to MXN$6.045 trillion in 2025, Hacienda informed. VAT revenues advanced 9.1%, IEPS 54.2% and import/export taxes 16.8%.

Banco de México’s deputy governor José Gabriel Cuadra considered it important to adopt a “wait-and-see” approach at the February monetary policy meeting. He expects this year’s tax adjustments to have a transitory effect, which would not generate additional monetary policy pressures.

The Mexican economy will grow 1.5% in 2026 and 2.1% in 2027, according to the IMF’s most recent World Economic Outlook report. This compares against 1.5% and 2.0%, respectively, in the previous WEO report.

CETES auction: 28-day CETES +1 bps to 7.00%; 91-day CETES -3 bps to 7.10%; 182-day CETES +7 bps to 7.26% and 350-day CETES +6 bps to 7.50%.

Download PDF: Mexican Market Chatter January 15th – 22nd