Mexico FinTech News

Keep Your Friends Close and Your Enemies Cashless? Oxxo and Nubank End Withdrawals Agreement

Femsa might be rethinking its fintech strategy, but for now it will have less to do with Nubank: after a 14-month partnership, Nu’s customers will no longer be able to withdraw cash at Oxxo stores; cash deposits will remain available. The company did not specify which party decided to end the agreement, or if it was a mutual decision, but Nu immediately announced that it will reimburse users for two monthly withdrawals from any bank ATMs (during March and April, at least, subject to extensions), so it clearly is seeking to mitigate the impact on its customers. Interestingly, OXXO withdrawals are still available to Mercado Pago users, as well as those of most legacy banks, for the same MXN 20 fee Nu users previously paid, so this would seem for now a Nu-OXXO issue. (Further, Nu is maintaining its cash withdrawals from other retailers, such as Chedraui, Soriana.) Given that Nu and OXXO CEOs know each other well and are said to get on, the decision to part ways on cash withdrawals would not have been taken lightly. (Both are in their mid 40s, Stanford MBAs, Millennial CEOs of top companies in a region where almost all other CEOs are mostly Boomers or maybe Gen Xs – even if Velez created Nu from scratch, while the highly qualified Fernandez, son and grandson of previous Femsa CEOs, was long destined to run the family-controlled business).

Nu México press release, 12/03/26: We are making adjustments to our cash-out network.

BBVA Mexico: Playing Offense from a Position of Strength

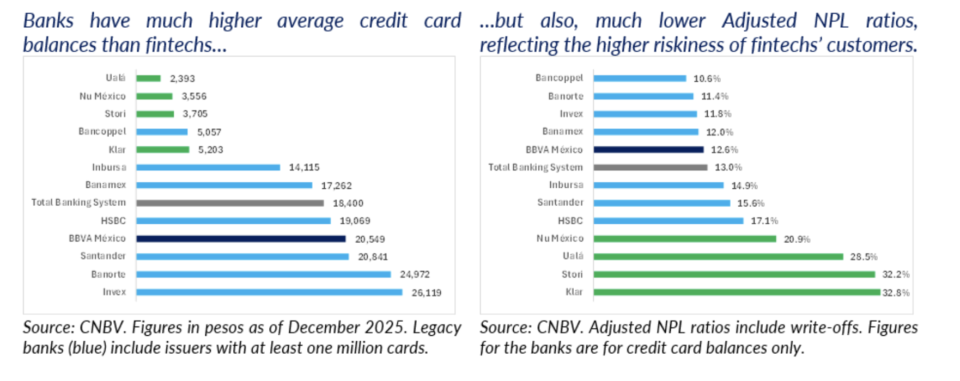

In a presentation in Madrid to analysts and investors, BBVA provided insights on its 2025-2029 strategic plan, focusing on companies and on Mexico, which in 2025 accounted for half of its consolidated net income. An optimistic view on the macro and that it leads the market in almost all segments will have come as a surprise to virtually nobody that is vaguely familiar with the bank’s Mexican operations. Nonetheless, we found some of the details on its evolution over the past years quite interesting, allowing the bank to become, in its own words, Mexico’s largest fintech.

It’s not just that BBVA México has kept on lending (though, clearly, that’s certainly part of it: it has grown its market share since 2018 in every category, except auto loans): the bank’s significant investments in technology have helped it nudge customers to digital platforms, with digital customers growing at a CAGR of 15% over the past six years, nearly tripling since 2019.

But perhaps the most telling figures came from credit cards, the segment that has seen the greatest competition from fintech challengers: in 2025, BBVA México issued some 2.7 million cards, of which only 22% were in the “open market”, that is, customers with which it didn’t already have a banking relationship. In absolute terms, this growth is close to Nu México’s 3.1 million; in percentage terms, Nu is evidently growing much faster, but there’s another key difference: Nu has previously stated that about half of its customers are first-time card users, so starting credit limits must be lower, as risks are much higher. CNBV figures confirm this.

(For context, if BBVA’s credit card portfolio had the same adjusted NPL ratio as Nu, it’d result in a reduction of close to 15% of its 2025 pre-tax income, all else equal.)

That is not to say that BBVA hasn’t faced challenges of its own, perhaps most notably back in October of last year when its “hyper-personalized” new app was launched to decidedly mixed reviews. Moreover, as fintechs move away from a credit card-only model to a wider service offering, competition is bound to increase across the board. Consumers will surely benefit (as they did from the fintechs’ aggressive yields on deposits); it’s much less clear who will win and who will lose on the corporate side.

Company press release, 10/03/26: BBVA Outlines Its Roadmap for Mexico Through 2029, Focused on Growth and Transformation | Webcast: Strategic Talks: Enterprises & BBVA Mexico | Presentation.

Ualá Launches U.S. Stock Investing in Mexico, Joining a Rather Crowded Room

Neobank Ualá announced a partnership with U.S.-based DriveWealth to launch Acciones, a new feature allowing Mexican users to invest in U.S. stocks and ETFs directly through its app. The service enables fractional investing starting from MXN 20 through DriveWealth’s regulated brokerage infrastructure, which handles execution, clearing, and custody. The launch aims to lower barriers to international investing in Mexico, where only 4.4% of the population currently invests in financial instruments, according to the CNBV. Nonetheless, there is no shortage of competition in the sector, including full service brokers (most notably GBM and Actinver in the retail market) and new entrants with diverse business models, such as Mercado Pago (through its partnership with GBM), Webull (which acquired a licensed broker) and Fintual (with a no-frills, fully online model).

Global FinTech Series, 11/03/26: DriveWealth Powers Ualá’s Launch of U.S. Stock Investing in Mexico.

Openbank Reignites Mexico’s Digital Savings Rate War with 13% Yield

Santander’s digital bank Openbank raised the yield on its Open+ debit account to 13% annually for balances up to MXN 40,000, reviving competition for deposits in Mexico’s fast-growing digital savings market. The move increases the previous rate from 9% and positions Openbank alongside fintech players such as Nu and Mercado Pago, which also offer 13% returns but with lower caps near MXN 25,000. The bank introduced a tiered structure: balances above MXN 40,000 earn 7.3% up to MXN 1mn and 7% beyond that level. By leveraging Santander’s balance sheet to offer high promotional yields, Openbank intensifies the battle between traditional banks and fintech platforms for retail liquidity, reinforcing a key strategy in the country to attract users through capped high-interest savings products.

El Cronista México, 10/03/26, Karla Tejeda: Openbank challenges fintechs in Mexico and rekindles a “rate war” with 13% and a new MXN 40,000 cap.

Konfío Prepares to Become a Bank and Expand SME Financial Services in Mexico

SME lender Konfío is in the final stage of obtaining its banking license, a move that would allow the fintech to expand beyond lending into deposits, payments, and treasury management for SMEs. The company currently operates as a tech-enabled SOFOM, and aims to build a unified platform where SMEs can access credit, manage payments, and hold deposit accounts in one ecosystem. Konfío says more than 80% of its clients receive their first business loan through the platform, highlighting its role in serving firms without collateral or banking history. With institutional funding already secured, the company plans to deploy roughly MXN 44 bn in loans over the next three years to about 85,000 businesses, reinforcing its strategy of combining credit expertise and technology to deepen financial access for SMEs.

Latam Fintech Hub, 13/03/26, Staff: Konfío, a Mexican SME lending fintech, prepares to become a bank and expand its services in the country.

Additional reading…

LatAm FinTech News

Nubank Hires Former TikTok Executive to Lead Global Marketing as Expansion Accelerates

Nu Holdings appointed former TikTok and Google executive Kim Farrell as global marketing director, signaling Nubank’s push to expand beyond Latin America and build a stronger international brand. Farrell will oversee global brand strategy, partnerships, and marketing campaigns, reporting to co-founder Cristina Junqueira, who leads the company’s U.S. operations.

TechStock², 10/03/26, Khadija Saeed: Nubank appoints former TikTok executive Kim Farrell as it accelerates its U.S. and global expansion.

Mercado Libre to Invest US$3.4bn in Argentina to Expand Logistics and Fintech Ecosystem

Mercado Libre announced it will invest US$3.4 bn in Argentina in 2026, a 30% increase from the US$2.6 bn deployed in 2025, to expand logistics infrastructure, strengthen its e-commerce platform, and deepen the growth of its fintech arm Mercado Pago. The plan includes building new fulfillment and storage facilities, improving technology capabilities, and hiring about 1,900 employees, bringing its local workforce to roughly 16,700. The investment reflects Mercado Libre’s strategy to scale both commerce and digital financial services across its ecosystem, using Mercado Pago to drive financial inclusion and support millions of consumers and SMEs.

El Economista, 12/03/26, Staff: Mercado Libre announces a US$3.4bn investment in Argentina for 2026

Nubank, WeBank and MYBank Lead Global Digital Banking Ranking as Sector Matures

Nubank, China’s WeBank and MYBank ranked as the world’s top three digital banks in the 2026 TABInsights World’s Top 100 Digital Banks ranking, The report shows digital banks entering a more disciplined phase after years of rapid expansion, with stronger balance-sheet management, diversified revenue streams and improved operational efficiency. Nubank retained the top spot due to strong customer growth (reaching 131 mn users by 2025), high engagement and a low-cost operating model, while continuing to expand internationally. The ranking also highlights widening gaps between leading digital banks and smaller peers. It outlined that scale, funding advantages, and diversified product ecosystems increasingly determine competitiveness in the global digital banking market.

The Asian Banker, 13/03/26, Wendy Weng: Nubank, WeBank and MYBank top the 2026 World’s Best Digital Banks Ranking with strong financial performance and diversified offerings.

Kushki Expands LatAm Payments Infrastructure Through New Partnerships

Kushki announced strategic partnerships with payment orchestration platforms Akurateco and Spreedly to strengthen infrastructure for merchants and payment service providers operating in Latin America. The integrations combine Kushki’s local acquiring network and regional financial services with global orchestration technology. The infrastructure would enable international merchants and PSPs to enter the region through a single integration while improving authorization rates and payment routing. The collaborations aim to reduce the operational and regulatory complexity of Latin America’s fragmented payments ecosystem, helping global companies scale to digital commerce in the region.

FF News & Mundo Ejecutivo, 11–12/03/26: Spreedly, Akurateco and Kushki Announce Strategic Partnership to Expand Payment Capabilities for PSPs Across Latin America

Additional reading…

- PicPay launches an eSIM & an investment aggregator using Open Finance to simplify asset management in Brazil.

Global FinTech News

Revolut Secures Full UK Banking License, Unlocking Lending Expansion

Revolut achieved a milestone when it recently obtained a full UK banking license, after going through more than a year of regulatory review. The license will allow the fintech to operate as Revolut Bank UK Ltd. and expand its services beyond payments into lending and deposit-taking in its home market. The approval enables Revolut to migrate UK customers to the new banking entity and offer products such as credit cards, loans, and savings under a fully regulated structure. The move marks major progress in the company’s strategy to deepen its banking capabilities and strengthen its position as a global digital bank, amidst intensifying competition between fintech expansion in regulated lending markets.

Bloomberg, 11/03/26, Aisha S Gani: Revolut set to win full UK banking license, paving the way for lending expansion.

Ripple Launches $750mn Share Buyback at $50bn Valuation

Ripple launched a $750 mn share buyback that values the blockchain payments company at $50 bn, reinforcing its position among the world’s most valuable crypto firms despite recent volatility in digital asset markets. The tender offer will allow employees and early investors to sell shares through April and follows Ripple’s broader expansion strategy, including acquisitions aimed at building infrastructure in brokerage and stablecoins. The move signals confidence in the company’s long-term growth as it seeks to diversify beyond cross-border payments and strengthen its role in the evolving global crypto and digital payments ecosystem.

Bloomberg, 11/03/26, Rebecca Torrence and Olga Kharif: Ripple launches US$750mn share buyback at a US$50bn valuation.

London Overtakes New York and San Francisco as World’s Leading Fintech Hub

London has surpassed San Francisco and New York to become the world’s largest fintech hub, driven by strong growth in European fintech investment and a slowdown in funding for major U.S. centers. Data from growth capital firm Finch Capital revealed a 37% increase in European fintech funding between 2022 and 2025 (to reach €40 bn) matching total funding in the United States after a 13% decline. The shift highlights Europe’s growing strength in regulatory-focused fintech segments such as compliance and financial software. However, the report warned that the region still faces challenges in late-stage funding, where large investment rounds remain heavily backed by U.S. investors. Analysts say increased venture capital participation from European pension funds could significantly expand funding capacity and further accelerate the region’s fintech ecosystem.

Reuters, 12/03/26, Leo Marchandon: London overtakes San Francisco and New York as the top fintech hub, growth capital fund says.

Additional reading…

Download PDF: Mexico Fintech Chatter – 17.03.26