Mexico FinTech News

Credit & NPLs grow at SOFIPOs…

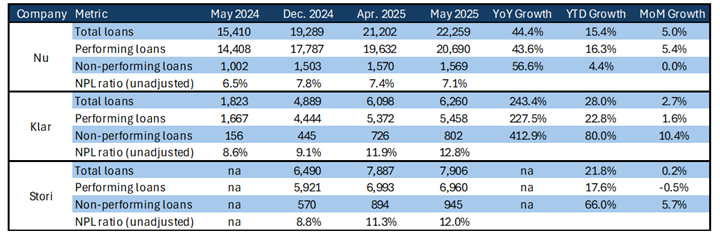

Condusef preliminary data for May showed Nu’s growth in loans regaining momentum, while Klar and Stori reported deteriorating NPL trends. Given the limited nature of the Condusef data, it’s not possible to fully determine yet underlying credit quality, with NPLs reduced by consistently high write-offs, especially at capital-heavy Nu. According to separate earlier CNBV data, as of March Nu’s adjusted NPL ratio (after write-offs) stood at 20.8%, just above Stori’s 17.1% and Klar’s 19.5%.

Source: Condusef. Figures in MXN million.

Bulls will argue this level of risk is normal, given these companies serve riskier customers. They also say growth matters more than profits right now, allowing fintechs to get the scale and data necessary to be profitable. Some even claim it’s unfair to judge them by bank standards, since their credit models are so different.

These are valid — or at least debatable — points. But over the years, many financial intermediaries have claimed they discovered a new way to lend profitably to people ignored by banks, only to find the reality of lending to the unbanked more challenging than they expected. Cynics point to current losses and argue that many of these consumer credit fintechs will end up the same way as their unsuccessful predecessors. Optimists say near universal smartphone and mobile data use, huge amounts of free unconventional data, AI, machine learning and the like will make this time different. All can agree that sooner or later the consumer credit card fintechs need to offer shareholders a decent return on equity if they are going to continue to be able to fund themselves.

Source: Klar’s Instagram account and Stori’s website. Screenshots taken on June 13, 2025.

…to the point that Banxico Urges Them to Exercise Caution in Issuing Credit Cards

The Mexican Central Bank has called on Sofipos such as Nu, Stori, and Klar to be more prudent in granting credit cards, citing rising delinquency in the sector. Governor Victoria Rodríguez emphasized that although funding is growing slower than deposit collection, credit expansion remains significant. The Financial Stability Report notes increased past-due loans despite higher charge-offs and write-offs. Banxico also confirmed it required Nu México to raise its initial capital to MXN 14.2 bn as part of its transition to licensed bank.

Bloomberg Línea, 12/06/25, Italia López: Banxico urges sofipos like Nu, Stori, and Klar to exercise caution in issuing credit cards.

CAME is Shut Down by CNBV

Financial regulator CNBV shut down operations at CAME, one of the largest Sofipos (which was nonetheless relatively obscure, as it pursued more of an old-school, offline strategy). An eventual liquidation process will be a major test to the Sofipo’s safety net, as well as a bitter reminder of its limits: savers with deposits in excess of MXN 212k (25,000 UDIs or about US$10k) will find their money above that threshold is uninsured.

BloombergLínea, 13/06/25, Michelle del Campo: Mexican regulator shuts down CAME.

Xepelin Secures US $15.75mn Credit Line from BBVA Spark

Chilean fintech Xepelin has secured a US $15.75mn credit line from BBVA Spark to expand its operations in Mexico. The funding will support the company’s mission to provide real-time financial services for SMEs, including digital payments, credit, and cash flow management tools. This marks Xepelin’s second credit facility in 2025, reinforcing its regional growth strategy and positioning in the B2B fintech space.

LatamList, 10/06/25, Araceli Dominguez: Xepelin secures US $15.75mn credit line from BBVA Spark

New Shareholder at Kueski: Attom Capital Joins

Kueski, Mexico’s BNPL and digital credit leader, has welcomed secondary-specialist Atom Capital as a new shareholder—likely via a secondary transaction. Founded in 2012, Kueski addresses Mexico’s lack of consumer credit by offering short-term cash loans and BNPL through major e-commerce partners like Amazon. With over 28 million loans issued and 90% repeat usage, it’s become key infrastructure in Mexico’s digital economy. Atom’s entry reinforces investor confidence in Kueski’s mission to bridge financial access gaps for Mexico’s middle class. Read more about how their product design fits real spending habits.

Attom, 12/06/25: Company press release.

BanCoppel Seeks to Add 3 mm Financial Customers Over Next Five Years

Amid the launch of a new corporate image for its holding company, BanCoppel’s management said the bank will seek to add more than three million customers in the next five years; the bank currently has about 14 mm customers. Part of the investment program announced (MXN 80 bn at the holding level) will be used to expand the bank’s physical presence, but also to boost its tech capabilities.

El Economista, 09/06/25, Edgar Juárez: BanCoppel Seeks to Add 3 mm Financial Customers Over Next Five Years.

Blog Post: Is Mexico’s Bank Licensing Window Quietly Closing?

In a column last week, El Financiero’s Jeanette Leyva sounded an alarm: Mexico’s long queue of fintechs hoping to become full-fledged banks may be in for a rude awakening. What once looked like a boom in digital banking has slowed to a bureaucratic crawl. Leyva reports that the CNBV — under Jesús de la Fuente — and Banxico — under Victoria Rodríguez — are now taking a much more cautious stance. Some, like Masari, Konfío, and Ion Financiera, are still in line. Others like Plata, Nu, and Revolut already have licenses but await final green lights to operate.

But the real chill came during a recent CNBV board meeting, where it was reportedly suggested that no new licenses be granted to current fintechs operating under alternative legal figures. The spotlight (not in a good way) turned to Klar, Finsus, and especially Mercado Pago — the latter criticized for offering crypto sales and its credit structure. Could this be true? Is the era of open-door digital banking over? For fintechs, the message seems clear: regulators are pumping the brakes. Ironically, just as fintechs seek to join the system, the system might be closing ranks. Could the Mexican authorities be foolish enough to deny Mercado Pago, part of the largest company in Latin America, a license while giving licenses to companies few people have heard of, and whose ultimate benefactors are far from well known? We actually doubt it, but the question is being asked.

El Financiero, 12/06/25, Jeanette Leyva: [Opinion column]: Tough outlook for those looking to become banks.

Covalto Targets Double-Digit Growth in SME Lending

Covalto’s CEO Mark McCoy emphasized that the bank’s focus remains exclusively on SME lending—not consumer credit—and that its data-driven digital approach gives it a competitive edge. Covalto expects to participate in the government’s “Plan México” through development bank guarantees. The bank has grown its loan portfolio by 30%, outpacing the single-digit growth of the broader banking sector. As of April, Covalto had MXN $8.18bn in deposits—doubling year-over-year—largely due to high-yield accounts offering double-digit returns on two-year terms. While 40% of clients arrive seeking credit, 60% come for its savings products.

Expansión, 12/06/25, Staff: Covalto, the fintech that bought a bank, targets double-digit growth in SME lending.

Kapital Bank Upgraded Credit Rating from Moody’s

SME FinTech Kapital Bank has been upgraded to A–.mx (long term) and ML A‑2.mx (short term) by Moody’s Mexico, with a stable outlook. This rating reflects the bank’s strong performance in the SME segment, successful digital integration, and consistent financial growth since its late-2023 acquisition. Deposits have surged to MXN 17.3 billion, credit portfolio rose from MXN 2 billion to MXN 7.6 billion, and non-performing loan rates remain low (3.1%) . Moody’s forecasts continued stability over the next 12–18 months. CEO René Saúl credits the achievement to solid capitalization, tech-driven services, and SME-focused strategy.

El Financiero, 11/06/25, Staff: Kapital Bank receives positive rating from Moody’s.

Additional reading…

LatAm FinTech News

Trii Reaches Break-Even; Eyes Expansion to Mexico in 2026

Colombian investment fintech Trii has reached break-even after raising new funding from U.S. venture firm Crestone, bringing its total capital raised to US $9mn. With over 500,000 users and US $300mn in AUM, Trii will complete its first EBITDA-positive quarter in June 2025. The company plans to enter the Mexican market in 2026, initially exploring personal investment offerings. Trii currently operates in Colombia, Peru, and Chile, where it has processed over US $1bn in trades since launching in 2021.

Bloomberg Línea, 11/06/25, Daniel Salazar Castellanos: Colombian fintech Trii reaches break-even and plans expansion to Mexico in 2026

Additional reading…

- Is Nubank still a good investment? Global fund labels its stock a “thermometer” for Latin America.

- Brazilian fintech Justa acquired by BTG Pactual to expand B2B offering.

- Frente raises US $5.5mn in Series A.

Global FinTech News

Chime Climbs 37% in Market Debut on Nasdaq

Chime, the San Francisco-based online banking platform, surged 37% in its first day of trading on Nasdaq, closing at US $37 after pricing its IPO at US $27—above the projected range. The company raised approximately US $700mn, with an additional US $165mn from secondary share sales. Chime reported a Q1 2025 net income of US $12.9mn and revenue of US $519mn (up 33% YoY). Founded in 2012, Chime has raised US $2.3bn to date, backed by investors such as DST Global, Crosslink Capital, and Menlo Ventures.

Crunchbase News, 12/06/25, Joanna Glasner: Chime climbs 37% in market debut on Nasdaq .

Walmart and Amazon Are Exploring Issuing Their Own Stablecoins

Merchants including Walmart and Amazon are exploring how to issue stablecoins, potentially shifting the high volumes of cash and card transactions that they handle outside the traditional financial system and saving them billions of dollars in fees, according to people familiar with the matter. With vast networks of customers and employees, troves of data and far lighter regulations, retail and technology companies have long been viewed as particular threats to banks, including regional and community lenders. The retailers’ final decisions would depend on a bill, called the Genius Act, which would begin to establish a regulatory framework for stablecoins. The bill recently passed another procedural hurdle but still needs to clear the Senate and House.

The Wall Street Journal, 13/06/25, Gina Heeb, AnnaMaria Andriotis and Josh Dawsey: Walmart and Amazon Are Exploring Issuing Their Own Stablecoins .

Additional reading…

- Marqeta to power new Klarna debit card in the U.S.

- Deutsche Bank and Ant International partner to expand payment services across Europe and Asia.

- Octaura raises US $46.5mn to give traders a way to trade loans more easily.

- Atome secures US $75mn financing to drive financial inclusion mission in the Philippines.

Download PDF: MI-MxFintechChatter-061625