Mexico FinTech News

Interchange Fee Cap Proposal Paused: Issuers Win the Battle (For Now)

Banking regulator CNBV is said to have formally halted, for now, the review of its joint proposal with Banxico to cap maximum debit and credit card interchange fees, citing the need for an “exhaustive and in‑depth analysis of the market”. At first glance, this reads like a victory for the banks and fintechs that mounted an aggressive lobbying campaign against the initiative, which was expected to have a material negative impact on their results. Just a little over two weeks ago, top bankers met with President Sheinbaum, who urged them to step up credit underwriting – a familiar request, as Mexican banks have prioritized stability over portfolio growth since the 1994 Tequila Crisis triggered a wave of bankruptcies. This time, however, Sheinbaum and team have identified a clear pain point that will give them explicit leverage should lending fails to reach the pace they want (of note, the withdrawal does not cancel the initiative, with CNBV explicitly reserving the right to reintroduce it). And some speculate the banks have agreed to voluntarily reduce average interchange fees, especially on debit cards, to fend off the official caps. Meanwhile various newspaper columnists have reported that the new Competition Watchdog (CNA) is going to block VISA’s acquisition of Prosa, one of two main switches that routes, authorizes and clears a large share of Mexico’s debit and credit card transactions between banks, acquirers and merchants.

El Universal, 13/02/2026, Antonio Hernández: CNBV takes a step back | Other Sources: El CEO | Dinero en Imagen.

Condusef January Loan Data: Noisy Start of the Year as Sofipos Adopt IFRS 9

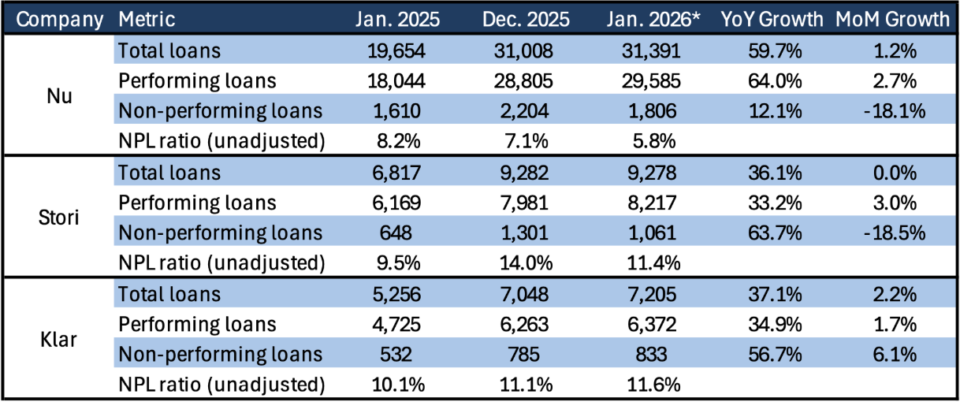

Preliminary loan data from financial consumer watchdog Condusef showed a relatively strong start of the year, with performing loans increasing MoM by 2.7% at Nu, 3.0% at Stori and 1.7% at Klar. However, we note figures are not fully comparable to last year’s, as Sofipos were required to adopt IFRS 9 starting in 2026, which changes how loans are classified between performing (now referred to as Stage 1 and 2) and non-performing (now Stage 3). In fact, we note Nu updated its submitted figures after some sell-side reports highlighted a sharp increase in NPLs, originally reported at 9.9% (a notable deterioration from 7.1% in December), subsequently updated to 5.8% (which could signal a notable improvement, though without write-off data, no firm conclusions could be derived); interestingly, the reported total portfolio remained unchanged at MXN 31.4 bn, up 1.2% sequentially.

In short, if under normal circumstances Condusef limited data only allowed for, well, limited conclusions, this month it probably only helps to encourage Nubank to be more forthcoming about its Mexican business: if analysts and investors will dig through official filings to get a sense of results, you might as well give them more details, so you can better control the narrative.

And for those wondering if there’s a way to make the numbers more comparable to pre-IFRS 9 figures, the short answer is no. When banks adopted it in 2022, some, like Banorte, provided figures for 2021 under both methodologies: some lines looked a little better, others looked a little worse.

Source: Condusef, CNBV, Miranda Partners. Figures in MXN million. * Figures starting in 2026 follow IFRS 9.

Source: Condusef, CNBV, Miranda Partners. Figures in MXN million. * Figures starting in 2026 follow IFRS 9.

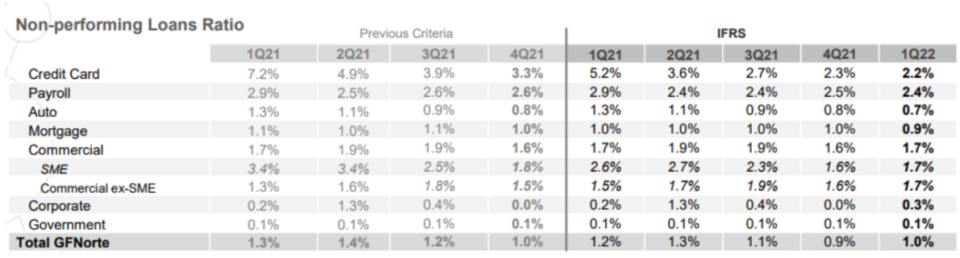

Banorte’s disclosure shows there’s no clear way to make pre- and post-IFRS 9 figures comparable

Source: Banorte 1Q22 earnings call presentation.

Nu Commits plans to have invested US$4.2 bn in Mexico 2020 – 2030 Ahead of Banking Launch

In a recent promotional videocast, Nu said it expects to have invested a total of US$4.2 billion in Mexico between 2020 and 2030 as it prepares to begin operating as a full‑service bank in 2026, subject to final regulatory approval. The figure unusually explicitly bundles both OpEx and CapEx in an overall number and includes the past 6 years of losses, but if that is what it takes to obtain a $4.2bn investment headline so be it. About US$2.5 billion is framed as ‘’investment’’ over the next four years, on top of capital already deployed. Nu Mexico’s CEO Armando Herrera commented in seven years Nu has gone from under 1 million to 13 million customers in Mexico, now claiming to rank fifth in the financial system (a somewhat dubious claim, based presumably on number of clients, and not by assets, equity or revenues as would be more standard metrics) and third in number of credit cards, adding roughly 1 million customers per quarter and 2 million in the past six months. The capital will help Nu compete with both incumbents and digital challengers by scaling its tech platform, growing its credit book, strengthening its balance sheet and regulatory buffers, and entering deposits and lending as a bank with meaningful funding capacity from day one. The North Korean style videocast (Question: “For sure, and I know we have a great, great team working on this tirelessly. And they’re really great. They’re top‑notch talent.”) also stresses Nu’s inclusion story. Around 22% of its customers previously operated only in cash, roughly 6 million people received access to credit for the first time via “La Moradita”, and half of Nu’s clients now hold their first‑ever credit card with the company. Nu has built a network of more than 30,000 cash‑in and cash‑out points, with around 75% of transactions being cash‑in, effectively converting physical cash into digital balances at scale and making cash its main competitor. Products like savings “Cajitas” are said to be central: they let customers see compounding yield in real time while keeping funds liquid, shifting deposits from mere transactional balances to genuine savings.

Nu Videocast: Mexico CEO Armando Herrera. | Other sources: El Economista, 11/02/2026, Edgar Juárez: Nu’s investment in Mexico will reach $4.2 bn by 2030.

Mexico’s New Tax Regulation Puts Crowdfunding at Risk and May Reduce Competition

Mexico’s 2026 fiscal reform is increasing pressure on crowdfunding platforms by requiring them to withhold 20% ISR and 16% VAT on interest paid to individuals, raising operational costs and reducing investor returns. Industry representatives argue the measure was implemented without a gradual transition, forcing platforms to invest heavily in technology upgrades and compliance, with some questioning the viability of their business models. The higher effective tax burden, compared to banks and brokerage firms, has already reduced investor appetite, with expected yields falling from 16.5–20% in 2025 to 15–18% in 2026. As 27 licensed platforms and nearly MXN 15 bn in loans have been placed since 2024, the sector warns that disproportionate tax treatment could accelerate consolidation, limit competition, and slow financial inclusion, despite authorities’ ongoing efforts to seek technical adjustments.

Expansión, 12/02/26, Luz Elena Marcos Méndez: New Tax Regulation Puts Crowdfunding at Risk and May Reduce Competition.

Azteca offers Actinver FI fund to its 23mn customers

Actinver and Banco Azteca are quietly positioning themselves against the GBM–Mercado Pago alliance by going after millions of small-ticket investors. On 9 February 2026, they launched Fondo Azteca 1 (AZTECA1), a medium‑term debt fund managed by Operadora Actinver and distributed 100% via Azteca’s app, targeting its base of over 23 million clients. Clients can invest from MXN$1, with daily liquidity, and the bank aims to reach 200,000–250,000 investors and around MXN$5 billion in AUM in the first year. The product blends Mexican government debt with high‑grade corporate bonds, using Actinver’s existing regulatory and operational infrastructure. But GBM has struggled so far to convert its 5.5mn active accounts into meaningful profitability, and presumably similar questions will be asked of the Actinver-Azteca alliance, although at a planned 250,000 clients it will be much smaller.

Expansión, 9/02/26, Luz Elena Marcos Méndez: Banco Azteca offers investment fund.

Additional reading…

LatAm FinTech News

Agibank Raises US$240 mn in New York IPO as Brazilian Fintech Listings Reopen

Brazilian digital lender Agibank raised US$240 mn in a New York IPO, selling 20 mn shares at US$12 each. The company reached a valuation of about US$1.92 bn, signaling a cautious reopening of U.S. capital markets for Brazilian fintechs. The offering was priced at the bottom of its revised range after being downsized, reflecting disciplined investor demand amid mixed post-IPO performance in the sector, and quickly traded below IPO, to close Friday at $11.0/s. Recently IPOed PicPay is also trading well below its IPO price. The Agibank deal highlights renewed but valuation-sensitive selective access to global capital for LatAm fintechs, as investors prioritize sustainable growth, profitability paths, and realistic valuations over aggressive expansion narratives.

Bloomberg, 10/02/26, Cristiane Lucchesi and Rachel Gamarski: Agibank Raises $240 Mn in New York IPO as Brazilian Fintech Listings Resume.

Pix Poised to Capture 50% of Brazil’s E-Commerce Market by 2028

Brazil’s instant payment system Pix is projected to account for 50% of the country’s e-commerce transactions by 2028, up from 42% in 2025. In addition, it is expected to surpass credit cards and widen its lead to 14 percentage points, according to Ebanx. Launched by Brazil’s central bank in 2020, Pix has rapidly expanded from peer-to-peer transfers into consumer-to-business payments, representing 46% of total transactions in January and boasting new features, such as recurring payments. The system has pressured card networks like Visa and Mastercard in a market historically dominated by credit cards, although installment payments remain a key competitive advantage for cards in higher-ticket purchases. Pix’s growth underscores the strength of public digital payment infrastructure in Brazil and its expanding role in reshaping Latin America’s largest e-commerce ecosystem.

Reuters, 10/02/26, Marcela Ayres: Instant payment system Pix poised to capture half of Brazil’s e-commerce market by 2028

Nubank Confirms Argentina Presence with Buenos Aires Hub

The opening of a hub in Buenos Aires has been announced by Nubank, as part of a broader US$475 mn, five-year investment plan to expand its international office network. The move does not yet include retail banking operations, but positions Argentina as a regional talent and development base to support technology, recruitment, and long-term strategic growth. The fintech, which operates at scale in Brazil, Mexico, and Colombia, appears to be taking a cautious approach in one of Latin America’s most volatile banking markets, using the hub to engage local talent and regulators while assessing future expansion opportunities in the country’s competitive fintech ecosystem.

The Digital Banker, 09/02/26, Staff: Nubank confirms Argentina presence with Buenos Aires hub.

BTG Pactual Acquires 48% of Digital Lender Meutudo to Expand Retail Strategy

Up to 48% of Brazilian digital credit fintech Meutudo has been acquired by BTG Pactual in a transaction valuing the company at around R$1 bn. The deal emerges as part of BTG’s strategy to strengthen its retail banking presence and may eventually lead to BTG taking control, pending regulatory approval. Meutudo, which focuses on payroll-deducted private loans and INSS-backed credit, currently originates about R$2.5 bn in loans per month, with BTG previously providing over 80% of its funding. Founded in 2019 as a credit marketplace before shifting to in-house origination, the fintech has served more than 19 mn clients and received prior backing from Goldman Sachs Asset Management, which exits with this transaction. The move deepens BTG’s push into digital consumer lending and highlights ongoing consolidation in Brazil’s retail credit ecosystem.

Forbes, 12/02/26, Staff: Brazilian Digital Credit Fintech Meutudo Acquired 48% by BTG Pactual to Expand Retail Segment.

Additional reading…

Global FinTech News

MrBeast Acquires Fintech App Step to Expand into Financial Services

In an unexpected turn of events, YouTuber MrBeast acquired US-based financial services app Step, which serves 7 mn teens and young adults with credit-building, savings, and investment tools. The fintech, founded in 2018, will operate under Beast Industries, which recently secured a US$200 mn investment from Bitmine Immersion Technologies, as part of a broader strategy to expand into financial wellness. The move signals the growing convergence between creator-led brands and fintech platforms targeting Gen Z audiences with digital-first financial products.

FinTech Futures, 11/02/26, Tyler Pathe: YouTuber MrBeast acquires financial services app Step.

Grab Agrees to Acquire Stash Financial for Initial US$425 mn

Southeast Asia’s superapp Grab has agreed to acquire US investing platform Stash Financial in a deal that begins with the purchase of a 50.1% stake for US$425 mn in cash and stock, with plans to buy the remaining shares over three years at fair market value. Founded in 2015, Stash manages US$5 bn in assets for more than one mn users, offering a range of services such as retail investing, stock-reward debit cards, and workplace financial wellness tools. The acquisition expands Grab’s financial services portfolio as Stash is expected to contribute over US$60 mn in adjusted EBITDA by 2028.

FinTech Futures, 12/02/26, Tyler Pathe: Grab agrees to acquire Stash Financial for initial $425m.

Additional reading…

Download PDF: Mexico Fintech Chatter – 16.02.2026 vGG