MARKETS

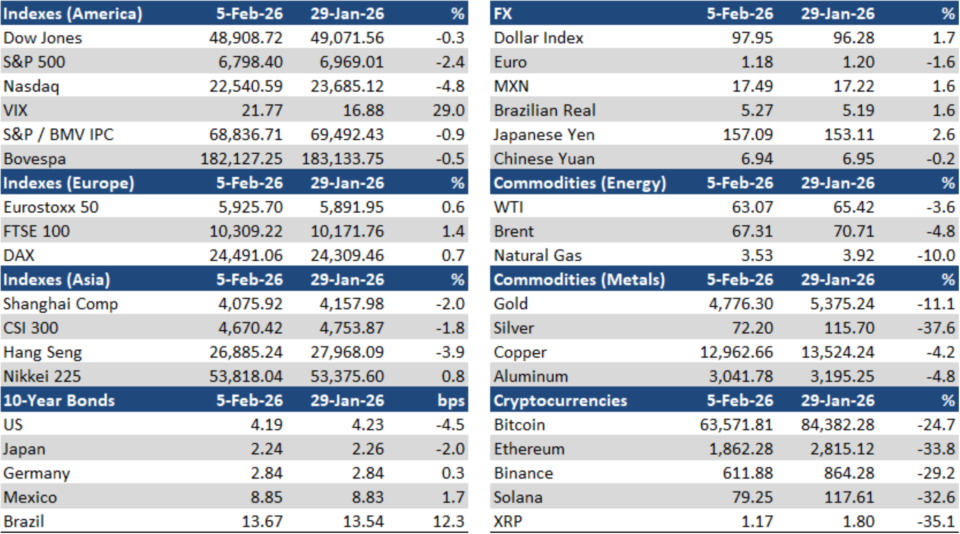

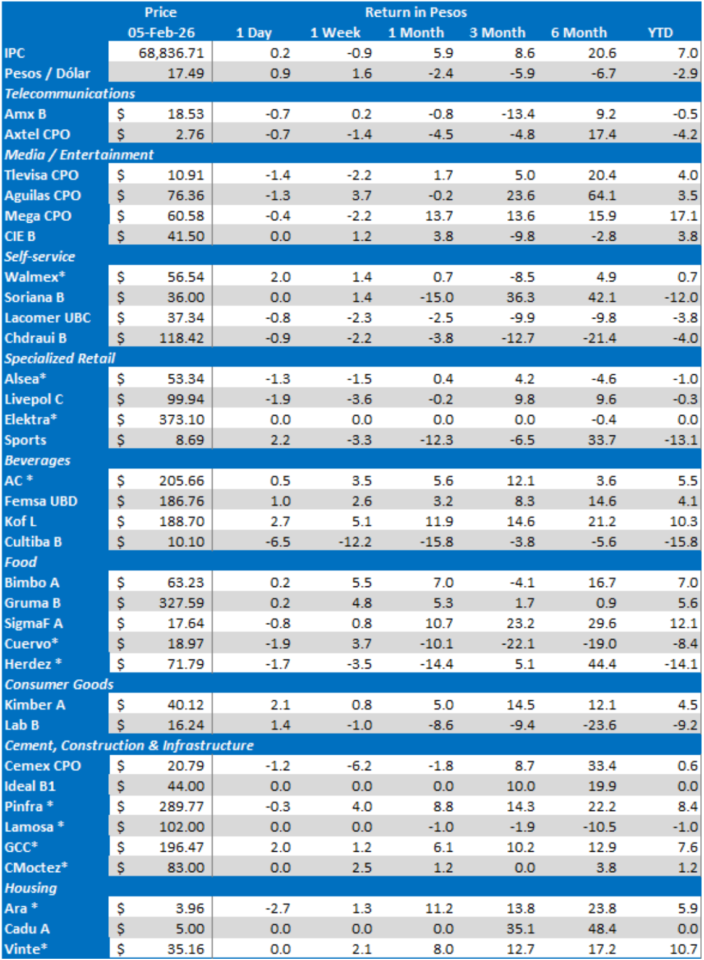

The S&P / BMV IPC experienced some profit taking (-0.9%) over the previous week dragged down by the correction in US equity indexes. Meanwhile, the Mexican peso lost 1.6% to close at MXN$17.49/USD; the yield of the 10-year M-Bono was up 2 bps to 8.85%.

The S&P / BMV IPC’s top gainers were: BIMBO A (+5.5%), KOF UBL (+5.1%), and GRUMA B (+4.8%). On the other hand, the main losers were: PEÑOLES * (-12.3%), CEMEX CPO (-6.2%) and GCARSO A1 (-3.9%).

LISTED COMPANIES

Cemex reported positive 4Q25 results. Consolidated sales were up 11% YoY (4% like-to-like), underpinned by strength in Mexico and EMEA. Consolidated cement volumes rose 1% YoY (Mexico -1%, EMEA +7%, U.S. -3%), ready-mix volumes eased 3% YoY, and aggregates volumes increased 2% YoY, with U.S. aggregates up 10% amid capacity additions and the Couch Aggregates consolidation. Prices strengthened materially in Mexico (cement +17% YoY) and advanced in EMEA (cement +10%), while U.S. cement pricing declined 3% amid competitive pressures, with ready-mix and aggregates price dynamics comparatively steadier. Consolidated EBITDA grew 16% YoY (9% like-to-like) and EBITDA margin widened 0.8 PP to 18.7%, reflecting the combined effect of pricing, efficiencies, and stronger operational performance in Mexico through 2H25. Net income swung to a loss versus a profit a year ago due to goodwill impairment and asset write-down. Free cash flow from operations declined 2% YoY. Net debt fell 15% YoY and the consolidated leverage ratio improved to 1.63x, from 1.81x. For 2026, the company expects a high single digit EBITDA growth, US$900 million in maintenance Capex, US$300 million in growth Capex, US$210 million in investments in intangible assets and a US$50-100 million investment in working capital. Cemex will further reduce its leverage levels to between 1.5-2.0x debt to operating cash flow, with the goal of maintaining a solid BBB rating and further improve its risk profile. The company will propose the payment of a US$180 million dividend in March with a 40% increase and a US$500 million share buyback program over three years.

GFInbur posted soft 4Q25 results. The loan portfolio increased 4.5% YoY driven by retail growth, particularly auto, payroll and credit cards, while the NPL ratio remained stable at 1.5%. Deposits advanced 8.2% YoY on retail inflows, while digital transactions reached 95.8% of total activity. Capital strength remained solid with a CET1 ratio of 23.6%. The financial margin fell 2.6% due to lower interest rates. Provisions rose 7.6% YoY leading to a 4.1% reduction in the risk adjusted financial margin. Net fees and commissions were down 8.6%, market-related income remained negative because of valuation effects, and non-interest expenses grew 4.9% YoY, keeping the efficiency ratio at a best-in-class 17.4% for the year and 16.6% in the quarter. Net profit declined 19.2% YoY due to an extraordinary MXN$1.4 billion VAT expense at the insurance subsidiary, resulting in an 11.5% ROE.

El Puerto de Liverpool reported preliminary 4Q25 results. The company estimates consolidated revenue growth between 6.5-6.9% for 2025, and between 4.8-5.2% in 4Q25. Same-store sales growth was approximately 4.2% in 2025 for both Liverpool and Suburbia, and 3.3% in Q4 2025 for both. This performance was driven by the successful execution of promotional campaigns such as “El Buen Fin” and “Night Sales,” complemented by solid growth in the Financial and Real Estate divisions. Liverpool anticipates that margins for the fourth quarter and the full year 2025 will show a slight contraction compared to the previous year, due to a decrease in gross trading margin, which incorporates higher logistics costs resulting from the change to the new Arco Norte location, an increase in operating expenses, and a more conservative approach to allowances for doubtful accounts. Regarding its stake in Nordstrom Inc., the company will recognize in 4Q25 an impact from accounting adjustments related to the allocation of the purchase price (PPA), as well as transaction costs, between US$170-175 million. Non-performing accounts receivable (NPA) levels (more than 90 days past due) will end the year in the range of 3.6% to 3.8%, compared to the 3.2% reported at the end of 2024. Next February 10th, Liverpool will issue US$500 million in 5.75% Senior Unsecured Notes due 2038 in the international markets. The notes are guaranteed by its subsidiary Distribuidora Liverpool, S.A. de C.V., carry investment-grade ratings of BBB from S&P Global and BBB+ from Fitch Ratings, and the net proceeds will be used to refinance the LIVEPOL 16 bond.

Quantum Energía (operator of the Fibra E-Fiemex plants) reported neutral 4Q25 results. Consolidated revenues of US$559 million for the quarter, up 18.0% YoY driven once again by higher average prices, as energy volume rose 8.5% to 12,240.4 GWh. The largest contributions came primarily from Tamazunchale I (+55.6%), La Laguna (+39.8%), Monterrey (+36.9%), and Escobedo (+35.7%), which offset declines in La Venta (-53.2%), Topolobampo II (-26.9%), and Tamazunchale II (-25.5%). The portfolio’s availability factor improved by 4.5 PP to 93.0%, supported by the Comprehensive Improvement Plan and lower overall unavailability, with 2.1% planned unavailability and 4.9% unscheduled shutdowns, despite isolated incidents at La Venta, Topolobampo II and III, and Tamazunchale II. The dispatch factor increased by 7.4 PP to 66.6%. Gross profit fell 11.7% YoY to US$188 million due to a 42.3% increase in gas supply costs, while the gross margin contracted to 33.6%, from 44.9%. EBITDA decreased 6.5% YoY to US$118 million, and the EBITDA margin closed at 21.0% (down 5.5 PP), given the less favorable energy cost environment that outweighed the benefit of lower operating, maintenance, and other costs. Fibra-E Fiemex will increase its debt by US$400 million of which US$300 million will be aimed at an extraordinary Capex program and the remained US$100 million for letters of credit to buy natural gas.

Banco Santander México reported strong 4Q25 results. Total loan portfolio grew 10.6% YoY, supported by robust commercial momentum across corporates, financial institutions, government entities and SMEs, plus double-digit expansion in secured retail (auto and mortgages). Asset quality improved, as the NPL ratio fell 27 bps YoY to 2.04%, while provisions declined 3.4% YoY on better performance in mortgages and corporate books. Deposits increased 7.3% YoY, led by demand deposits (+9.0% YoY) and stronger individual sight balances (+8.3% YoY), consistent with a more efficient funding mix. Digital activity remained a key pillar, with digital clients up 6.9% YoY and digital channels accounting for 74% of total sales. Net interest income rose 9.9% YoY and NIM expanded 18bp YoY to 5.37%, as a sharper drop in interest expense than in interest income more than offset a lower-rate environment. Operating expenses advanced 4.5% YoY on personnel, D&A and taxes, partly offset by lower technology spend, while the efficiency ratio improved 250 bps YoY to 43.50%. Net profit increased 25.8% YoY and ROE expanded 206bp YoY to 19.94%.

Grupo Salinas agreed to pay MXN$32 billion to the tax authorities, of which MXN$25 billion will be paid by Grupo Elektra. The latter amount includes an initial disbursement of approximately MXN$6.5 billion, and the remainder MXN$18.5 billion in 18 monthly installments.

Fibra Next instructed the Trustee to transfer and issue 120,835,869 CBFIs, in compliance with its contractual obligations and as part of the contribution process, including the portfolio known as Júpiter Adicional.

Grupo Aeroportuario del Pacífico’s total passenger traffic declined 2.2% YoY in January, with Mexico traffic down 1.2%, Montego Bay falling 37.7% and Kingston decreasing 6.9%.

Grupo Aeroportuario de Centro Norte’s total Passenger traffic grew 6.0% to 2.3 million in January. Domestic traffic rose 7.0% while international traffic rose 1.4%.

CFECapital announced that the rate for voltage greater than or equal to 220 kilovolts will be P$0.0607 for generators and P$0.0791 for consumers, or the entities responsible for the load, down 0.98% and 0.38%, respectively, compared to the 2024 rates. The rate for voltages below 220 kilovolts will be P$0.1110 for generators and P$0.1801 for consumers, or the entities responsible for the load, with no changes in the first case and a 0.1% decrease in the second.

Femsa has completed the separation of the Grupo Nós joint venture in Brazil with Raízen. As a result of this transaction, Femsa retained the OXXO stores in Brazil, as well as the distribution center located in Cajamar, São Paulo. Grupo Nós’ remaining assets and liabilities have been allocated between Femsa and Raízen in accordance with their business.

Banregio Grupo Financiero carried out the spin-off of part of Banco Regional’s assets, liabilities, share capital and certain active and passive operations, which were transferred to a spin-off company that will merge with its digital Hey Banco.

Grupo Herdez announced that Gerardo Canavati Miguel, is leaving his position of Chief Financial and Technology Officer to assume the role of CEO of McCormick de México. The company appointed Andrea Amozurrutia Casillas as the new Chief Financial and Sustainability Officer. Andrea joined Grupo Herdez in 2010.

Grupo Bimbo issued domestic bonds (Cebures) amounting to MXN$12 billion in two tranches: the first one for MXN$7.867 billion with a 9-year maturity and 9.22% fixed interest rate, and the second one for MXN$4.133 billion with a 4-year maturity and variable annual interest rate of TIIE +0.45%. This transaction a ‘mxAAA’ credit rating from S&P Global Ratings, and ‘AAA(mex)’ from Fitch Ratings. The company will use the proceeds to refinance existing debt.

Arca-Continental issued MXN$9.5 billion in domestic bonds (Cebures) in two tranches. The first one amounted to MXN$6.24 billion with a 7-year term and a fixed interest rate of 8.96%, and the second one amounted to MXN$3.26 billion with a 3-year term and a variable interest rate equal to the TIIE + 40 bps. Both issues received a “mxAAA” credit rating from S&P and “AAA(mex)” from Fitch Ratings.

Fibra Mty has successfully entered into a credit agreement with a syndicate of four banks, led by Banorte, for up to US$215 million. The credit facility includes an option to increase the amount by an additional US$50 million, for total commitments of up to US$265 million.

Volaris agreed to open 13 new routes from OMA’s airports during the first half of 2026. On the other hand, Volaris’ shares will likely substitute Becle in the upcoming March rebalancing of the S&P / IPC BMV, according to local brokers’ estimates.

Axtel reported weak 4Q25 results. Total revenues down 1% YoY, comparable EBITDA down 31% YoY, a comparable EBITDA margin contraction to 25% from 36% in 4Q24, and net income up 13% YoY. The quarter reflected solid Government segment growth that partially offset weaker Enterprise and Wholesale trends, while comparable EBITDA declined mainly due to an extraordinary provision reversal recorded in 4Q24, higher operating and personnel expenses, and an unfavorable comparison base. Net income improved supported by a significantly lower financing cost driven by FX gains and reduced interest expense following debt prepayments. For 2026, management guided revenues of MXN$12.85 billion and EBITDA of MXN$3.8 billion, with Capex of approximately US$83 million, while maintaining a focus on deleveraging, cash generation, and operational efficiency.

América Móvil will sponsor the new North American team Cadillac, which will debut in the 2026 Formula 1 season, according to local newswires.

Grupo Hotelero Santa Fé has reached an agreement for the purchase of a beach hotel in Ixtapa-Zihuatanejo with 70 rooms. The company did not provide the amount of this transaction, which is subject to obtaining the corresponding corporate and regulatory authorizations.

OTHER COMPANIES

Pemex’s CEO Víctor Rodríguez Padilla provided a summary of the company 2025 results. Pemex offset the decline in oil and natural gas fields and stabilized national production on an annual basis with an increase of 122,000 barrels per day. In refining, the company closed December 2025 with 1.5 million barrels per day of crude oil processing and registering a higher yield of over 60%. Pemex reduced its total debt by more than US$20 billion (-20.1%) against 2018, to the lowest level in the last 11 years. Payments to suppliers exceeded MXN$390 billion in 2025. In 2026, Pemex and the private sector will invest MXN$425 billion, representing a 34% increase compared to 2025. These funds will be aimed at ensuring production, efficiency, and sustainability in the medium and long term. The plan includes priority exploration and production projects such as Trión, Zama, and Maloob, to meet the goal of 1.8 million barrels per day; as well as strategic natural gas projects in Ixachi, Bakté, and Burgos, with the objective of reaching 4.5 billion cubic feet per day.

HSBC Mexico has appointed former Secretary of Finances José Antonio Meade Kuribeña as non-executive Chairman of the Board of Directors, effective February 3rd. Jorge Arce will remain as CEO of HSBC Mexico and Latinamerica CEO and Board Member.

Fintech Konfío will invest MXN$44 billion from 2026 to 2028 to provide credit to SMEs, in line with the objectives of the Plan Mexico. The company plans to invest an additional MXN$7 billion to strengthen its technological and compliance infrastructure, as well as to enhance its risk management capabilities and create formal, specialized jobs in the financial sector.

Clara renewed a US$150 million credit facility with Goldman Sachs. This renewal lifted the company’s total debt capacity to more than US$250 million, including facilities secured in 2025 from the IFC, Covalto, BBVA Spark and General Catalyst’s Customer Value Fund.

Digital bank Grupo Covalto appointed Sergio Arias as Chairman and Deputy CEO of Banco Covalto. Mr. Arias will work closely with Covalto’s co-founders and co-CEOs, David Poritz and Allan Apoj.

Nacional Financiera and Bancomext will provide up to MXN$120 billion in financing to micro, small, and medium-sized enterprises. These programs include reduced interest rates on factoring loans, as well as 70% guarantees for loans of up to MXN$20 million pesos in priority sectors and 80% guarantees for first-time loans of up to MXN$5 million pesos.

Dell Technologies inaugurated a new Solar Community Center in Zapopan, Jalisco, which will offer free access to technology, digital skills development, social services, and community meeting spaces.

ECONOMIC

Banco de México left its key interest rate unchanged at 7.0%, as broadly expected. The decision was unanimous. Going forward, the governing Board will evaluate additional adjustments to the reference rate, taking into account all inflation factors. The Central Bank also increased its 2026 inflation expectations to 3.5% (headline) and 3.4% (core), from 3.0% in both cases. It continues to expect the inflation rate to reach 3.0% by 2Q27 and to finish the year at that level.

4Q25 GDP grew 0.8% QoQ (seasonally adjusted) in real terms, which was above the 0.6% consensus expectation and the best quarter since 3Q24, INEGI reported. Both secondary and tertiary activities advanced 0.9% while primary activities were down 2.7%. As a result, 4Q25 GDP was up 1.6% YoY based on original data, which was also above the 1.3% consensus forecast and the strongest annual performance since 3Q24, led by a 5.3% rise in primary activities, a 2.0% increase in tertiary activities and a 0.4% advance in secondary activities. Total 2025 GDP grew 0.5% (original data), the lowest level in six years, with primary activities up 3.7% and tertiary activities advancing 1.2%, but secondary activities falling 1.3%.

Hacienda reported that the fiscal deficit, based on the Public Sector Borrowing Requirements and excluding support provided to Pemex, reached 4.3% of GDP in 2025, a reduction of 1.5 percentage points compared to the previous year, but slightly above the 3.9% originally approved by Congress. The Historical Balance of the Public Sector’s Borrowing Requirements (SHRFSP) stood at 52.6% of GDP, exceeding the 52% level reported at the end of 2024. Hacienda also stated that public sector revenues grew by 2.5% real in 2025 to nearly MXN$8.0 trillion with non-oil revenues increasing 3.3% and oil revenues declining 2.7%. Tax revenues rose 4.1%, with VAT revenues up 2.6%, income taxes advancing 3.7% and special taxes on production and services (IEPS) rising 2.6%. Meanwhile, public sector spending decreased by 1.8%.

ANTAD’s same store sales were up 3.1% in 2025 (self-service +1.3%, department stores +4.8% and specialized retail +3.6%), while total sales grew by 5.6% YoY (self-service +4.0%, department stores +6.3% and specialized retail +7.3%. In 2026, ANTAD expects an increase of 3.9% in SSS and 6.3% in total sales and a US$3.7 billion Capex (vs. US$3.3 billion in 2024) from its affiliates.

Private consumption declined 0.5% MoM (seasonally adjusted) in November, reversing the positive monthly performance of the last 5 months, according to INEGI. Demand for domestic goods increased 0.1% while imports were down 2.9%. However, private consumption grew 1.4% YoY (original date) with domestic goods rising 0.1% and imports up 7.8%.

Gross fixed investment grew 0.4% MoM in November 2025 on a seasonally adjusted basis, supported by a 1.5% increase in construction spending while machinery and equipment edged down 0.2%, according to INEGI. Gross fixed investment contracted 6.4% YoY (original data) as machinery and equipment investment fell sharply by 14.5% while construction was up 1.3%.

The Global Indicator of Business Confidence declined 0.2 points MoM and 3.4 points YoY to 48.0 in January, which was the eleventh month below the 50 level, according to INEGI.

Remittances increased 1.9% YoY in December to US$5.2 billion, after 8 months with annual reductions, according to Banco de México. Nevertheless, total remittances for the year fell 4.6% to US$61.8 billion.

Light vehicle sales increased 8.7% YoY to 131,472 units in January, according to INEGI.

Total credit in the banking system expanded 6.6% YoY In December 2025, according to the CNBV. It was supported by solid growth in corporate lending at 6.5% YoY, consumer credit at 12.8% YoY and housing loans at 5.5% YoY, while credit to financial entities increased 2.2% YoY and government lending contracted 5.1% YoY. The sector’s NPL ratio rose to 2.17%, from 2.02% a year earlier, while the coverage ratio declined to 148.4%, from 156.6% YoY. Monthly net profits reached MXN$304.4 billion, representing a 4.8% YoY increase. ROE moderated to 17.2%, from 18.2% YoY, while ROA remained stable at 2.0% compared with last year.

Total Assets Under Management of the Afore system increased 22% YoY in December 2025, led by Afore Sura (+28%), Afore XXI Banorte (+24%) and Afore Citibanamex (+20%), according to Consar data.

Economist continued to expect a 25-bps reduction in Banxico key interest rate cut at the May meeting, unchanged versus the prior survey, according to the latest Citi Mexico Expectations Survey. The policy interest rate is seen at 6.50% by YE26, stable relative to the previous survey, and 6.50% by YE27. GDP growth expectations improved marginally, as the 2026 forecast increased to 1.4%, from 1.3% in the previous survey, while the 2027 projection held steady at 1.8%. The headline inflation projection for YE26 remained at 4.0%, with the core component increasing to 4.1%, from 4.0% in the last survey. For YE27, headline inflation forecasts rose to 3.75%, from 3.70%, while the core inflation projection was marginally up to 3.71%, from 3.70%. Peso expectations strengthened to 18.35 by YE26, from 18.75 in the previous survey, and the YE27 forecast appreciating to 19.00, from 19.07 previously.

The Mexican government unveiled the “2026-2030 Infrastructure Investment Plan For Development with Well-being”, which includes public and mixed investment of approximately MXN$5.6 trillion over the 2026-2030 period to strengthen economic growth and social welfare by expanding capacity across eight strategic sectors including energy, trains, highways, ports, health, water, education and airports.

Mexico and the US agreed to implement an Action Plan on Critical Minerals with the goal of strengthening supply chains in North America, correcting distortions in global markets, and reducing vulnerability to disruptions and external pressures. This bilateral mechanism includes coordinated trade policies and potential price floors at the border for imports of critical minerals, according to the USTR.

Mexico’s investment portfolio reached a record high of nearly US$407 billion, driven by new projects in the 32 states, according to Economy Secretary Marcelo Ebrard.

CETES auction: 28-day CETES -5 bps to 6.90%; 91-day CETES -7 bps to 7.03%; 182-day CETES +1 bps to 7.15% and 364-day CETES -13 bps to 7.37%.

Download PDF: Mexican Market Chatter January 29th – February 5th