Noticias FinTech México

DolarApp raises US$70M and rebrands as ARQ to expand digital dollar platform

ARQ’s (formerly DolarApp) latest US$70 million round brings iconic VC funds Sequoia and Founders Fund onto its cap table, alongside Kaszek and others. The financing supports a shift from a “dollar wallet with a nice card” into a full-stack, hard-currency-centric financial platform for Latin America’s globally exposed middle and mass affluent. But naturally this will not be easy. This is a crowded space, with other larger FinTechs (especially Revolut, which inspired ARQ) and incumbents all moving in the same direction.

The company’s current scale, low-single-digit millions of users and double-digit billions in annualized volume, suggests it has already moved beyond the “stablecoin remittance hack” phase. ARQ now wants to become an operating system for cross-border income, spending and saving in a region where banking remains largely domestic, peso-anchored and technologically outdated. In positioning terms, it looks to be aiming for a space between regulated neobank Revolut (where the three founders worked) and Bitso’s crypto-first approach.

By avoiding full-bank regulation, ARQ can stay lighter, faster and less capital-intensive than a traditional bank. But if it succeeds in becoming a primary financial relationship at scale, it may eventually be pushed toward deeper regulation, adding exactly the cost, compliance burden and operational complexity it is currently designed to avoid. In that sense, part of the model’s appeal may prove temporary.

Revolut has shown this stack can work in Europe, but its move toward becoming a full bank in Mexico brings high costs and regulatory obligations. Bitso has demonstrated strong demand for stablecoin rails and dollar exposure, yet it is still perceived mainly as a crypto exchange rather than a core financial relationship. Meanwhile, traditional banks are also trying to build toward the same end state: multi-currency access, better FX, cross-border payments and broader investment functionality, even if they are doing so more slowly and with worse user experience.

ARQ’s thesis is that a large, underserved cohort of Latin Americans lives multi-currency, multi-jurisdictional financial lives, currently stitched together across remittance rails, local banks, FX brokers and international brokerages that were never meant to work as one system. That may be true—but the size and durability of this addressable market of mobile Latin American users is still not fully proven.

That uncertainty matters because multi-country banking stories in Latin America have generally performed poorly. Regional scale sounds compelling in theory, but different regulatory regimes, consumer behaviors, funding economics and compliance standards have repeatedly made cross-border banking platforms harder to build than investors expect. ARQ is trying to unify the stack—with crypto powering the backend, but kept largely out of the storefront—yet the history of the region suggests execution risk rises sharply once a company moves beyond a single product and a single market.

On the product side, ARQ retains DolarApp’s dollar- and euro-centric accounts while expanding into a broader multi-rail, multi-product platform. Users hold dollar and euro balances via stablecoins—a detail that could still be a dealbreaker for crypto-skeptics, even if it is familiar to anyone who has used Bitso or USDC. Funds can move between those balances and local fiat, mainly Mexican pesos, through an FX model marketed as tight and transparent compared with legacy bank spreads.

That base layer connects to international payments, both person-to-person and to bank accounts, through a simple fee structure that contrasts with the opaque pricing of traditional remitters and banks—and, in some corridors, with Wise’s still complex pricing grid. But simplicity at the front end does not eliminate complexity underneath: the product still depends on correspondent relationships, compliance controls and capital-markets plumbing that users do not see until something breaks.

ARQ is also now building a more bank- and broker-like stack on top of those rails: international cards, including a metal Prestige card; yield on dollar balances at money-market-like rates; and access to listed securities such as ETFs and stocks. The ambition is clear: turn balances into an everyday spending and investing relationship, essentially a mobile-first global brokerage embedded in the wallet. The challenge is that every additional layer makes the product more valuable, but also more operationally sensitive and more likely to draw regulatory attention.

The initial wedge—FX and dollar exposure—is clearly real. Mexico alone received about US$65 billion in remittances in 2024. A growing base of digital nomads, freelancers and founders paid from the US and Europe, along with the nearshoring boom, is increasing demand for hard-currency access. Across LatAm, upper-middle-income households are also looking for liquid savings and investment exposure in hard currencies and international assets without opening US brokerage accounts or relying on legacy private banks. Still, it is not obvious that this naturally becomes a mass-market, multi-country banking franchise rather than a valuable but narrower niche.

Wise is excellent at moving money along one rail, and Revolut is excellent at turning balances into multifunctional accounts, but neither has yet fully solved the LatAm mix of regulation, culture and dollar demand. ARQ is trying to translate those conditions into a synthetic USD-based checking, savings and brokerage relationship inside a single app, with expansion underway in Argentina, Colombia and beyond. The question is whether that becomes a defensible regional platform or another case where expansion logic outruns local execution.

There are, in any case, real risks. ARQ operates directly in one of the most sensitive areas of the financial stack: stablecoin-mediated cross-border flows, hard-currency savings and retail access to global assets. Early user narratives in app-store reviews and forums show the usual tension. When the product works, experienced users praise its UX and ease of moving money cross-border. Negative feedback clusters around support quality, unexpected limits and funds held during compliance reviews, with some users reporting blocked transfers after changes in correspondent banking relationships or discontinued compatibility with services like PayPal, and in some cases closing accounts over perceived reliability issues.

For investors, that is the key point. ARQ’s moat—if one emerges—will not be built only on consumer product design, but on the resilience and redundancy of its underlying banking and capital-markets infrastructure, and on its ability to manage compliance reviews and edge cases without eroding trust among users highly sensitive to capital controls and counterparty risk.

The new funding round—and the stature of the investors behind it—gives ARQ both runway and a much heavier expectation load. The market will judge it not just on growth, but on whether it can turn a globally mobile niche into a defensible multi-product franchise in a region where trust, compliance resilience and regulatory positioning will determine which entities succeed in becoming an operating system for money.

Bloomberg, 03/03/26, María Clara Cobo: Sequoia, Founders Fund back $70 million raise for Latam’s ARQ.

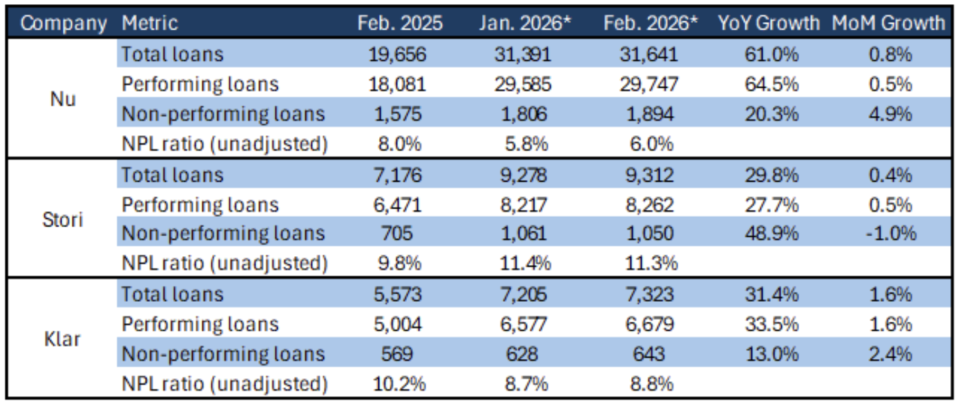

Condusef February Loan Data: Muted Growth, NPL Ratios Continue to Tick Higher

Preliminary loan data from financial consumer watchdog Condusef showed overall muted loan growth in February, a typically quiet month, with sequential increases impacted by the shorter duration. Nubank’s performing loans edged up 0.5% MoM, same as Stori’s; Klar (which like Nu, updated its figures for January, likely reflecting IFRS 9 implementation adjustments), had a faster clip, climbing 1.5%. Nu and Klar both saw slight sequential deteriorations in their unadjusted NPL ratios; as usual, we note that, without write-off data, it’s not possible to draw more meaningful conclusions about credit quality.

Source: Condusef, CNBV, Miranda Partners. Figures in MXN million. * Figures starting in 2026 follow IFRS 9.

Ualá Keeps Raising Funds as Mexican Operations Continue to Post Negligible Growth

Neobank Ualá announced yet another impressive funding round, raising in ‘’equity financing’’ US$195 mn from new and existing investors, led by Allianz X, the venture capital arm of insurance giant Allianz; the company says it is now valued at US$3.2 bn, up from US$2.75 bn in March 2025, cementing its status as one of the most successful fintech fundraisers in LatAm. (As often with Fintech raises, some skepticism may be warranted: is ‘’equity financing’’ pure equity, is $3.2bn valuation based on equity value of each share, or is this a convertible strike price, does this factor in negative effect on older shareholders of possible liquidity rights to new shareholders?). In any case, the fund raise stands somewhat in contrast to its results in Mexico, where its bank has continued to post significant losses (as most of its peers), but unlike them with rather little to show for in terms of portfolio growth. According to CNBV figures, in 2025 its consumer portfolio nearly tripled – but from a very small base: in absolute terms, it rose by only MXN 501 mn in the full year, from MXN 277 mn to MXN 778 mn, a tiny fraction of the MXN 11.7 mil millones Nubank grew in the same period, or even the MXN 2.8 bn from Stori or MXN 2.2 bn from Klar. Meanwhile, Uala’s Mexican losses in 2025 reached MXN 1,274 mn; seen another way, operating expenses of MXN 1,124 mn were more than 2x the year’s portfolio net origination. One hopes the new funds will help them achieve the much-promised but yet-to-materialize scale. To outsiders, the Mexico strategy remains largely a mystery.

Bloomberg, 04/03/26, María Clara Cobo: Ualá Reaches $3.2 Billion Valuation in $195 Million Round.

Lectura adicional...

Noticias de LatAm FinTech

From word-of-mouth virality to Messi’s new locality: Nubank secures new stadium’s naming rights

Back when it was gearing up for its IPO in 2021, Nubank bragged that the vast majority of its millions of users had come with virtually no marketing expenditures, relying instead on word-of-mouth and an impressively high net promoter score (NPS). The strategy changed when it entered Mexico, spending heavily on both online ads and billboards. The strategy will now see another step-function evolution: the company announced it has reached an agreement with Inter Miami’s to become the name sponsor of its new stadium; terms weren’t disclosed (usually not a sign of modest figures being involved). While we don’t question the marketing appeal of Lionel Messi, it’s tough to argue that this is not a harbinger of the much higher costs ahead, as the company keeps up its geographic expansion, particularly its entry in the United States. The investment might ultimate pay off if the company reaches a meaningful scale, but it’s clear the table stakes will be much higher.

The Athletic, 04/03/26, Paul Tenorio: Inter Miami’s new stadium to have Nubank as naming rights partner | Company press release: Nu and Inter Miami CF announce multiyear partnership.

Lectura adicional...

Noticias mundiales sobre tecnología financiera

Revolut applies for US banking license to accelerate expansion

London-based fintech Revolut has applied for a US banking license with the Office of the Comptroller of the Currency and the Federal Deposit Insurance Corporation as part of its strategy to expand in the world’s largest financial market. The company also appointed a former Visa executive as CEO for its US operations, signaling a more aggressive push into the country. If approved, the license would allow the firm to operate nationwide, offering regulated banking services across all 50 states. The move comes as Revolut, last valued at US$75 bn, seeks to scale its global digital banking model and compete more directly with traditional banks and fintech rivals in the United States.

Bloomberg, 05/03/26, Aisha S. Gani: Revolut Applies for US Bank License, Hires Former Visa Exec as America CEO.

SoftBank-backed PayPay targets up to US$13.4bn valuation in US IPO

In what could become one of the largest US listings by a Japanese firm, PayPay is targeting a valuation of up to US$13.4 bn in a planned US initial public offering, seeking to raise about US$1.1 bn. PayPay was founded in 2018 as a joint venture between SoftBank and Yahoo Japan, and has grown into one of Japan’s largest digital wallets with around 72 mn registered users, driven by incentives and merchant fee waivers that accelerated the country’s shift toward cashless payments. The offering, expected to list on Nasdaq under the ticker PAYP, is backed by cornerstone investors including units of Qatar Investment Authority, Visa, and Abu Dhabi Investment Authority expressing interest in purchasing up to US$220 mn in shares.

Reuters, 02/03/26, Arasu Kannagi Basil & Manya Saini: SoftBank-backed PayPay targets up to $13.4 billion valuation in US IPO.

Walmart-backed PhonePe targets up to US$10.5bn valuation in India IPO

Indian digital payments platform PhonePe, backed by Walmart, is targeting a valuation between US$9 bn and US$10.5 bn in a planned initial public offering that could raise around US$900 mn to US$1.05 bn, according to sources. As part of the offering, Walmart is expected to reduce its stake by about 12%, while early investors Tiger Global and Microsoft plan to exit their positions. PhonePe, one of India’s largest fintech platforms with more than 650 mn registered users, processed nearly 10 bn transactions on the country’s UPI instant payments system in January, representing almost half of total UPI volume. Despite its scale, investors remain cautious about the company’s ability to monetize its user base in a market where instant payments are free, highlighting broader challenges in building sustainable business models in India’s highly competitive fintech sector.

Reuters, 04/03/26, Jaspreet Kalra: Walmart-backed PhonePe targets up to $10.5 billion valuation in India IPO, sources say.

Lectura adicional...

- Santander and Mastercard complete Europe’s first live end-to-end payment executed by an AI agent

- Visa and Bridge Expand Collaboration, with Plans to Bring Stablecoin-Linked Cards to Over 100 Countries

Descargar PDF: Mexico Fintech Chatter – 09.03.2026