Noticias FinTech México

The Resurgence of a Mexican Unicorn: Kavak Raises US$300 mn Series F, $4bn+ valuation?

Kavak may be the only large Mexico startup to close various up-rounds culminating in a September 2021 Series E $700mn raise at a US$8.7bn valuation, then a big down-round in March 2025 with a raise of $127mn at a US$2.2bn valuation, and then last week another major up-round, maybe above $4bn. The company announced it has raised US$300 mn in its Series F, led by Andreessen Horowitz, which invested US$200 mn by itself, with investors including WCM Investment Management adding the remaining US$100 mn. The new valuation was not officially disclosed, but CEO Carlos García Ottati told Bloomberg it was higher than the most recent US$2.2 bn round. In this viral blog Luis Enríquez, a well-connected Partner from Nazca VC fund (the original pre-seed investor in Kavak and which seems to have helped arrange the a16z deal) wrote “This week, those same investors could have doubled their investment in less than a year”, suggesting a valuation over US$4 bn if accurate.

As Enríquez wrote in his blog, Kavak has gone through a profound and complementary AI and credit-driven transformation. Newly released data shows sales reached 120,000 units in 2025, up about 40% from the previous year. An expanding high margin portfolio of financial products has been key, with the company reaching consolidated monthly profitability for the first time in December. Indeed, Kavak’s fintech unit has financed more than $1 billion for customers since launch, and in Q4 2025 it was originating loans at an annualized run rate of about $600 million. Proceeds will be used to expand financing capacity and develop new fintech products, alongside further AI and technology investments, signaling that investors are again willing to back Kavak’s combined AI-first auto and financial-services play.

Kavak, 17/02/26, Company press release: Kavak announces USD$300 Million Series F led by Andreessen Horowitz to Expand Access, Trust, and Financing Across Latin America | Otras fuentes: Bloomberg.

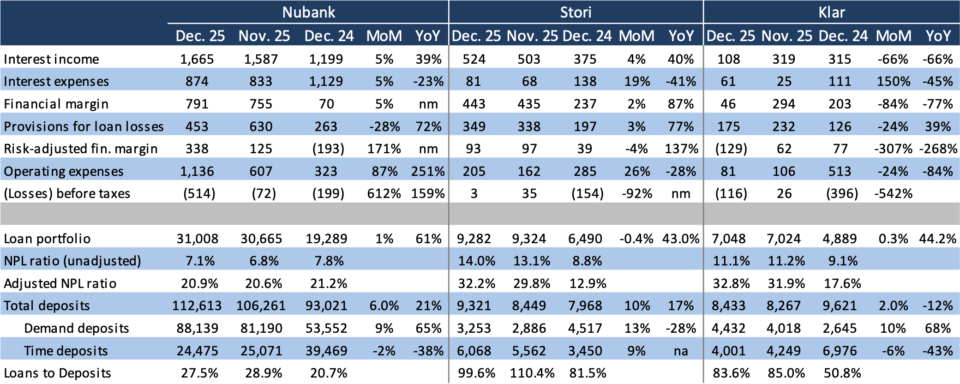

Sofipos’ December Results: High Expenses Offset Improvements in Financial Margin

CNBV released Sofipos’ financial results for December (portfolio data matched revelaciones anteriores de la Condusef). Trends were similar across the board, with declining interest expenses helping the financial margin, but surging operating expenses weighing on the bottom line; deposits also rose sequentially across the board, likely reflecting December’s year-end bonus (aguinaldo). In the case of Nu, the financial margin rose more than 10x, reflecting the benefits of both a normalizing loan-to-deposit ratio and lower reference rates; on the other hand, operating expenses nearly doubled MoM, leading to the largest loss before taxes since April 2025. Credit quality continued its gradual but steady deterioration, with the adjusted NPL up to 20.9%; write-offs for the year totaled MXN 5.4 bn, and pre-tax losses were MXN 3 bn.

Stori was the only one of the three that managed to report positive pre-tax results, though barely, at just MXN 3 million for the month. For the full year, pre-tax losses were MXN 175 mn, though a negative effective tax rate allowed for an accounting net profit of MXN 253 million.

Lastly, Klar (again) reported variations in its results, with interest income plunging 65% MoM (not explained in the data base; likely reflecting year-end adjustments; the company has not yet published its own quarterly report). Pre-tax losses for the year totaled MXN 506 mn.

Fuente: CNBV, Miranda Partners. Cifras en millones de MXN.

CNA Blocks Visa’s Acquisition of Prosa

The National Antitrust Commission (CNA) blocked Visa’s bid to buy a 51% stake in payment processor Prosa on the grounds that the deal would harm competition and users in the card payments ecosystem. According to the regulator, the transaction could have imperiled Carnet, the Prosa-owned brand that competes with Visa and Mastercard, mostly in prepaid cards used as food and gasoline vouchers. Moreover, it also argued it could reduce competition in the processing market, as both Visa and Mastercard are already licensed processors, even though the market is an effective duopoly split by Prosa and E-Global. Of note, the decision marked a significant change in regulatory view: Cofece, the CNA’s predecessor, had urged the divestment of both Prosa and E-Global, as it saw their control by banks as a risk to competition (Prosa is owned by Banorte, HSBC and Santander, among others, while E-Global is owned by BBVA and Banamex). Daniel Becker, head of mid sized bank Mifel, and former President of the ABM, argued in a provocative LinkedIn post that geopolitical concerns played a role. “At a time when data is the new oil, handing over the processing operation to an international player raised questions about technological sovereignty. Regulators and some shareholders understood that it was not only a financial decision, but a long-term public policy decision.” Behind the scenes, it is thought by some that Mexican regulators are punishing Visa for immediately cutting off international network access to Intercam and CI card holders after US sanctions were announced on those entities last year, instead of waiting for the sanctions to take effect. Columnist David Paramo reported that VISA and the selling banks will appeal the decision.

Bloomberg, 20/02/26, Amy Stillman and Paige Smith: Visa’s Takeover of Prosa Rejected by Mexico’s Antitrust Watchdog. | Otras fuentes: Dinero en Imagen.

EFEX raises $8mn to disrupt FX transfers

EFEX, a financial platform focused on global treasury and cross-border payments for mid-market companies, closed an $8 million seed round co-led by PayPal Ventures and Floodgate, with participation from Contour Venture Partners and Nido Ventures. The raise comes as fintechs claim SME corporate finance teams look for alternatives to legacy rails that they argue remain slow and expensive. (There is some standard FinTech gaslighting on this issue; traditional banks have in fact slashed fees and improved speed on FX, with some such as Santander now offering commission-free FX transfers). EFEX is positioning itself as a modern layer for companies that need to pay suppliers, collect locally, and manage multi-currency cash flows across both countries. CEO and co-founder Dimitri Zaninovich says the goal is to replace “used by habit” systems with a more efficient setup, using technology to automate operations and simplify treasury workflows. The company says it grew revenue sixfold in 2025 and processed more than $1 billion in payment volume, expanding teams and presence across Mexico’s main business hubs while preparing to scale further in Mexico and the United States.

LatAm Fintech Hub, 19/02/26: Fintech EFEX raises US$8 million in a seed round to strengthen its global treasury platform in Mexico and the U.S.

RIP Kubo, once a promising Fintech

Kubo Financiero, once one of Mexico’s storied fintech names, seems to be heading into a rescue-style merger with Crédito Maestro in a deal said to be valued at about MXN 610 million (roughly US$36 million). Kubo brings its CNBV-regulated Sofipo license and digital platform, while Crédito Maestro contributes capital and commercial reach. Recent figures cited in local reporting point to pressure at Kubo, including weak profitability, elevated delinquency, and below-average loss coverage. If regulators approve, the combined group would push beyond Crédito Maestro’s payroll-loan roots into a broader digital savings-and-credit play. For Kubo, it’s less a growth story than a rescue which hopefully will preserve jobs and at least some capital for its original shareholders.

LatAm Fintech Hub, 18/02/26: Kubo and Crédito Maestro advance US$35.6 million merger to strengthen their presence in Mexico’s digital savings and credit market.

Lectura adicional...

- Mexico’s Plata Wins Banking License, Heating Up Fintech Race.

- Credit booms in Mexico: card spending jumps 20% and 61 million cards now in circulation

- Rappi co-founder launches 30X in Mexico, a program to help entrepreneurs scale up to 30 times.

- Belvo unveils its AI-powered Open Finance ecosystem to transform financial services in Mexico.

- Finsus joins the UN Global Compact and launches green loans in Mexico.

- Chilean fintech Cenit enters Mexico to transform tax management for individuals.

- 30% of Mexicans turn to loan apps to cover financial emergencies.

Noticias de LatAm FinTech

Visa to Acquire Prisma and Newpay from Advent to Strengthen Argentina Payments Infrastructure

Visa looks set to expand its footprint into Argentina’s financial infrastructure, with its agreement to acquire Prisma and Newpay from Advent International. The companies are both payment platforms within the South American country: Prisma processes more than six bn transactions annually for major banks; Newpay, on the other hand, operates ATM and electronic bill payment networks. The acquisition builds on Visa’s regional strategy of integrating local platforms to accelerate tokenization, biometric authentication, and AI-driven risk tools, reinforcing its role in modernizing Argentina’s digital payments ecosystem amid ongoing industry liberalization.

Reuters, 19/02/26, Arasu Kannagi Basil: Visa to buy payment firms Prisma, Newpay to deepen Argentina footprint.

LatAm Fintech IPO market looking fragile after weak performance of PicPay, Agibank

Brazil’s and LatAm’s long‑awaited fintech IPO window is already looking fragile, as the first two deals of the year are casting a shadow over the sector. PicPay, the J&F (Batista family) fintech, priced in New York at the very top of its range — US$19 per share — only to slide roughly 20% below the offer, leaving the stock in the mid‑US$15s last week. Agibank (AGI), the second offering of the year, initially targeted 43.6 million shares at US$15–18, but the bank had to cut the deal size by more than half and trim the range to US$12–13. It ultimately priced at US$12, the bottom of that revised range, and opened on the NYSE down, closing last week just back at issue. Investors appear skeptical of cash‑burn‑driven growth or stretched forward multiples which may prompt some IPO‑ready names to delay listings rather than accept terms that would sharply reset their private marks.

Reuters, 11/02/26: Brazilian fintech Agibank raises $240 million in scaled-back US IPO

Listo Raises US$191.5 mn via FIDC to Scale Automotive Credit Platform in Brazil

Listo, a Brazilian automotive fintech, raised R$1 bn (US$191.5 mn) through two consecutive FIDC issuances structured by Itaú BBA and UBS BB, to expand its credit portfolio and strengthen operations. Of the total, R$700 mn represents new capital, while R$300 mn comes from existing investors extending maturities. Founded in 2014, Listo manages a loan portfolio of R$1.5 bn (US$287 mn) and processes about R$10 bn (US$1.9 bn) in digital transactions each year for more than 120,000 auto dealers and parts retailers across Brazil. The company has raised roughly R$3 bn through nine FIDC issuances to fund its growth.

Latam Fintech Hub, 17/02/26, Finsiders Brasil: Listo, a Brazilian automotive fintech, raises US$191.5 million through an FIDC to expand its portfolio and strengthen its operations.

Brazil’s Central Bank Liquidates Banco Pleno Citing Liquidity Deterioration and Regulatory Breaches

In the latest development tied to the Banco Master fraud investigation, Brazil’s Banco Pleno SA and its affiliated brokerage have been liquidated. The Brazilian central bank, which carried out the act, cited regulatory breaches and liquidity deterioration. While Pleno accounted for just 0.04% of system assets, its links to Master have already led to the liquidation of related entities, including fintech-controlled institutions. The move affects around 160,000 creditors, with up to R$4.9 bn (US$938 mn) potentially covered by Brazil’s deposit insurance fund (FGC), putting additional pressure on the country’s financial safety net.

Bloomberg, 18/02/26, Matheus Piovesana: Brazil regulator liquidates bank with ties to Banco Master.

Lectura adicional...

- Chilean fintech Global66 seeks an international banking license to expand its financial services across multiple countries.

- Brazilian fintech Laqus acquires Estar.finance and targets the secondary market and digital assets.

- Fintech TokenOne receives authorization from Brazil’s Securities and Exchange Commission to operate as a crowdfunding platform.

- Peruvian fintech Monnet Payments launches Virtual Accounts to offer a unified regional payments infrastructure.

- Lyra Colombia launches Send, its new infrastructure to automate mass payments and transform corporate treasury.

Noticias mundiales sobre tecnología financiera

Klarna’s stock collapse casts cloud over BNPL

Klarna’s fourth-quarter print is casting a broader shadow over the BNPL industry by reminding investors that, at scale, these platforms still behave like credit businesses with funding costs, processing costs, and operating leverage that can cut both ways. The company’s quarterly revenue topped $1 billion for the first time (up 38% year on year to $1.08 billion), but it also swung to a $26 million net loss versus a $40 million profit a year earlier, and it issued 2026 guidance that came in below expectations. Management argued the miss reflects the timing of growth costs being booked upfront, with revenue and profit arriving later as growth normalizes. Public markets did not buy the near-term tradeoff: the stock dropped about 23% on the day to a record low around $14.53, extending a steep decline since the September IPO and reinforcing how quickly sentiment can turn when growth is accompanied by rising costs and softer forward signals.

Reuters, 19/02/26, Supantha Mukherjee: Sweden’s Klarna swings to loss as fast growth hikes costs, shares fall 23%.

Stripe’s Bridge Receives Conditional US Bank Charter Approval to Expand Stablecoin Services

Stripe’s stablecoin unit Bridge received conditional approval from the US Office of the Comptroller of the Currency to become a national trust bank, allowing it to operate stablecoin products under direct federal oversight once fully approved. Stripe acquired Bridge for US$1.1 bn last year to integrate stablecoin infrastructure into its payments ecosystem. As a result, clients have been able to issue tokens, launch stablecoin-linked cards, and manage accounts funded with digital dollars. Bridge joins firms such as Circle, Ripple, BitGo, Fidelity Digital Assets, and Paxos in securing preliminary trust charters, reflecting a shift toward regulated crypto-finance integration. The move follows new US stablecoin legislation and highlights growing convergence between fintech, banking charters, and digital asset infrastructure. Stablecoin issuers, meanwhile, seek formal entry into the US banking system.

Bloomberg, 17/02/26, Emily Mason: Stripe’s Bridge joins crypto firms securing nod for bank charter.

Robinhood Files US$1 bn IPO for Retail-Focused Private Markets Fund

Robinhood is looking to raise US$1 bn through the IPO of Robinhood Ventures Fund I, a closed-end fund structured to give retail investors access to late-stage private companies before they list publicly. The vehicle will offer 35 million shares at US$25 each and already holds stakes in Databricks, Oura, and Revolut, with a planned investment in Stripe. Unlike traditional mutual funds, the closed-end structure means shares may trade at a premium or discount to the value of underlying assets, adding a market-driven dynamic to private exposure.

Bloomberg, 17/02/26, Natalia Kniazhevich and Anthony Hughes: Robinhood’s $1 billion fund pitches pre-IPO stock as next craze.

ECB Estimates Digital Euro Rollout Could Cost Banks €4–6 bn Over Four Years

An estimation from the European Central Bank warns that implementing the digital euro would cost euro zone banks between €4 bn and €6 bn over four years. The ECB itself expects setup costs of about €1.3 bn, with ongoing operational expenses near €300 mn per year. Under the proposed model, banks would distribute the digital euro through apps and recoup their investment via merchant fees, while the ECB would not charge for use of its network. Merchant fees would be capped below current card network levels, creating incentives for adoption. The ECB is selecting lenders for a pilot phase ahead of a planned 2029 launch, positioning the digital euro as a tool to modernize payments, reduce reliance on non-EU providers, and strengthen the bloc’s monetary sovereignty.

Reuters, 19/02/26, Valentina Za: Digital euro to cost EU banks 4-6 billion euros over 4 years, ECB estimates.

Lectura adicional...

- Vestwell raise headlines $1.29bn week as FinTech funding momentum builds.

- Apollo-backed fund lends US$250 million to Wayflyer to finance SMEs.

- Biggest African economies lead stablecoin demand growth, study shows.

- Revolut Business launches ‘360’ merchant acquiring solution, debuting in the Australian market.

- Philippine Fintech Maya Is Said to Weigh US IPO of Up to $1 Billion.

Descargar PDF: Mexico Fintech Chatter – 23.02.2026