MERCADOS

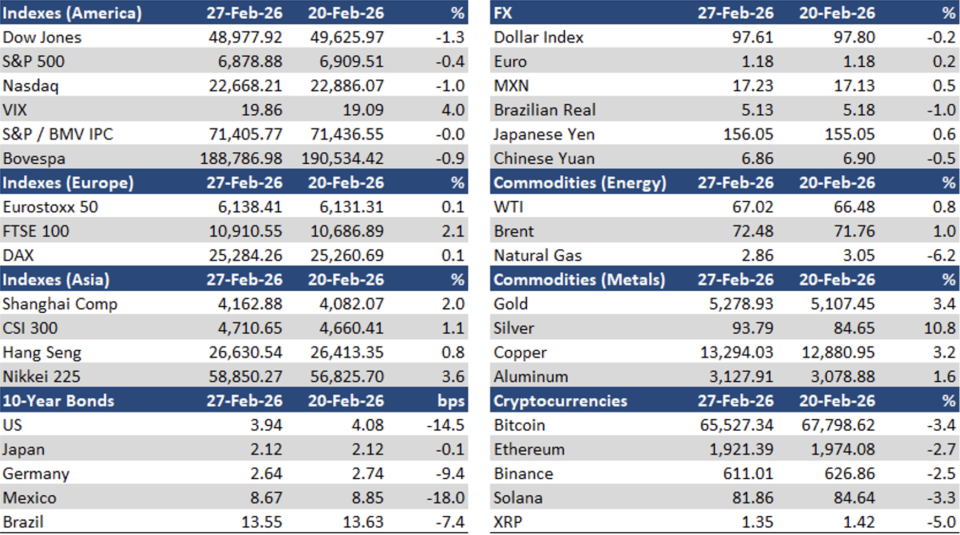

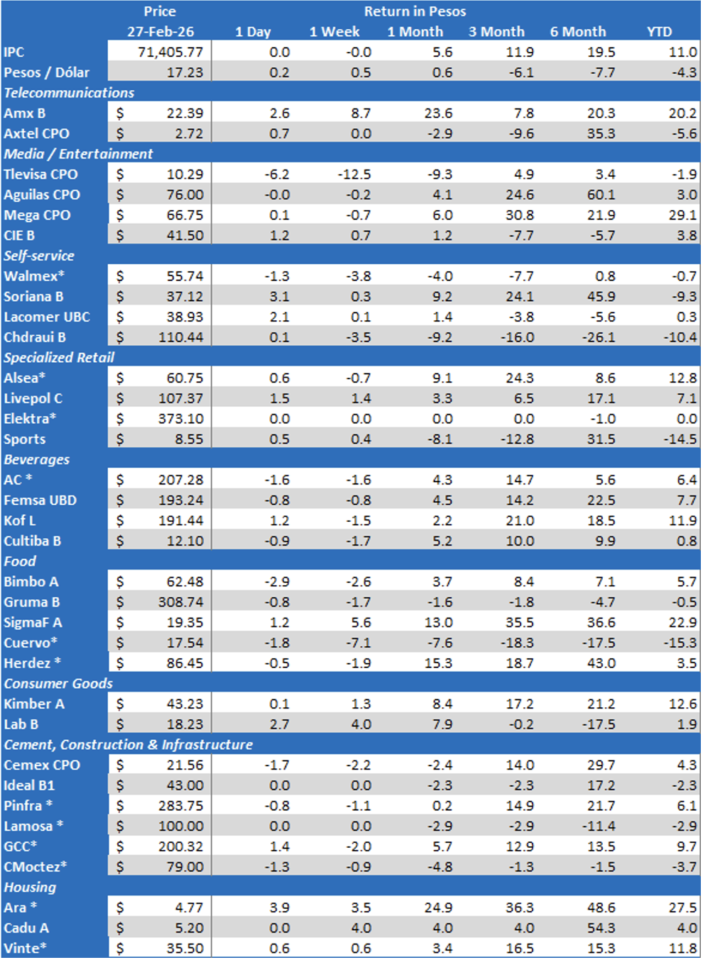

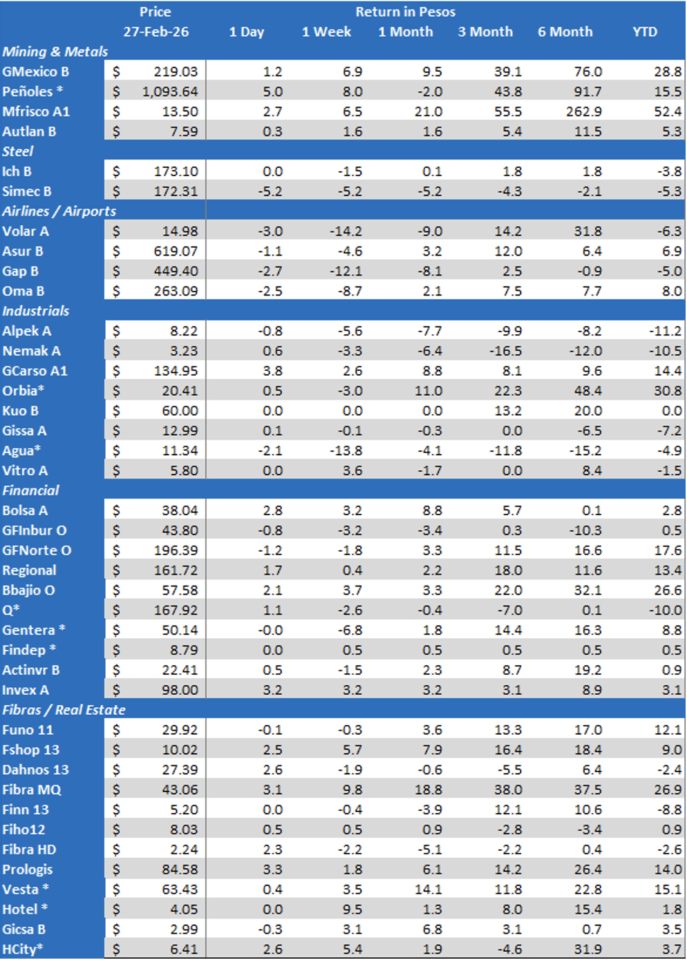

En S&P / BMV IPC remained stable over the week amid mixed quarterly results and macroeconomic data. Meanwhile, the Mexican peso lost 0.5% to close at MXN$17.23/USD; the yield of the 10-year M-Bono was down 18 bps to 8.67%.

En S&P / BMV IPC's top gainers were: AMX B (+8.7%), PEÑOLES * (+8.0%), and GMEXICO B (+6.9%). On the other hand, the main losers were: TLEVISA CPO (-12.5%), GAP B (-12.1%) and OMA B (-8.7%).

EMPRESAS COTIZADAS

Citi agreed to sell another 24% equity stake in Banamex to various institutional investors and family offices including General Atlantic, Afore Sura, BTG Pactual, Chubb and some funds managed by Blackstone, Liberty Strategic Capital and Qatar Investment Authority, for MXN$43 billion with a 0.85x P/BV valuation. The individual equity stakes do not exceed 4.9% of the company. Citi does not foresee additional divestitures in 2026.

Fibra Prologis and Macquarie Asset Management México (“Macquarie”), have entered into a binding Transaction and Covenant Agreement (the “TCA”) under which Macquarie has agreed to transfer to Prologis all of its rights and obligations under the management agreement entered into between Macquarie and Fibra Macquarie (the “Macquarie Management Agreement”), subject to the satisfaction of certain conditions. The sale of the management rights is conditioned upon, among other customary conditions, the acquisition in a tender offer by Fibra Prologis of at least a majority of the outstanding real estate trust certificates (“CBFIs”) of Fibra Macquarie not held by Macquarie. The tender offer will be for up to 100% of the outstanding CBFIs issued by FIBRA Macquarie. Under the TCA and in connection with the management rights sale, an affiliate of Macquarie that owns Fibra Macquarie CBFIs has agreed to sell, subject to certain conditions, its CBFIs to Fibra Prologis at the tender offer price. For such purposes, FIBRA Prologis has made a filing to obtain all required governmental approvals, including from the Mexican Banking and Securities Commission (Comisión Nacional Bancaria y de Valores), and intends to launch a tender offer and exchange transaction for up to 100% of the outstanding Fibra Macquarie CBFIs at a fixed exchange ratio of 0.525 Fibra Prologis CBFIs for each Fibra Macquarie CBFI, or an amount in cash equal to MXN$40.00 per Fibra Macquarie CBFI, up to a maximum total cash amount of MXN$7.973 billion, which is equal to 25% of all outstanding Fibra Macquarie CBFIs as of February 24, 2026, and which offers the holders of the CBFIs issued by Fibra Macquarie a premium to the 60-day volume-weighted average price as of February 24th, 2026 close of approximately 20% on a blended basis. Fibra Prologis intends to launch the tender offer in the second quarter of 2026, subject to obtaining the required corporate and regulatory approvals. FibraPL reported neutral 4Q25 results. Total portfolio GLA increased 32.7% YoY, reflecting the full-period consolidation of Terrafina, while average occupancy declined 130 bps YoY to 97.0%, driven by higher vacancy in selected manufacturing markets. Total revenues decreased 0.5% YoY, affected by FX translation and a tougher comparison base. FFO rose 11.8% YoY, supported by same-store NOI growth and acquisition contributions, while the FFO margin expanded 90 bps YoY. AFFO increased 16.0% YoY, reflecting operating leverage and disciplined capex, with the AFFO margin improving 140 bps YoY. LTV closed at 25.1%, down 30 bps YoY, underscoring balance sheet strength. Key quarterly developments included incremental sponsor acquisitions, the near-complete integration of Terrafina, and the successful issuance of a US$500 million international bond to refinance short-term debt and extend maturities. For 2026, management guided to occupancy above 96%, positive same-store NOI growth, net absorption of approximately 28 million square feet, and stable leverage, positioning the platform to continue benefiting from structural nearshoring demand.

Nu Holdings reported a strong 4Q25, with the total credit portfolio expanding 40% YoY driven by sustained loan origination momentum across Brazil, Mexico, and Colombia, while total customers increased 15% YoY to 131 million supported by continued penetration gains and product launches, and the activity rate remained broadly stable at ~83%, confirming high engagement. Asset quality improved, as the 15–90 day NPL ratio declined 10 bps YoY to 4.1% reflecting disciplined underwriting and favorable seasonality, while deposits grew 29% YoY, outpacing portfolio growth and keeping the loan-to-deposit ratio conservative. Total revenue rose 45% YoY, above market expectations, driven by higher monetization and ARPAC growth of 45% YoY, while gross profit increased 38% YoY and gross margin expanded on operating leverage. Credit loss allowance expenses remained well controlled, consistent with the improvement in NPLs, supporting net profit growth of 50% YoY, which exceeded expectations, and a record ROE of 33%.

Mercado Libre delivered mixed 4Q25 results with higher-than-expected revenue growth but margin compression due to free-shipping. Net revenues and financial income rose 45% YoY and accelerated versus 3Q25’s 39%, driven by sustained scale gains across Commerce and Fintech and strong execution in Brazil and Mexico, while Argentina normalized as inflation eased. Commerce revenues advanced on logistics density and value proposition enhancements, with FX-neutral GMV growth of 35% YoY in Brazil, 35% YoY in Mexico with fulfillment penetration approaching 80%, and 42% YoY in Argentina after stabilizing versus 3Q25 volatility. GMV increased 36.8% YoY and re-accelerated sequentially versus 3Q25’s 28%, reflecting higher items sold and broader category engagement. Unique active buyers reached 83 million, up 24% YoY, while loyalty strengthened as MELI+ adoption improved frequency and retention. Fintech services sustained momentum with MAU of 78 million, up 28% YoY, supported by wallet penetration and acquiring growth, particularly in Mexico. The credit portfolio expanded 90% YoY, NPLs edged up to 7.6%, and the NIMAL spread widened sequentially to 23.3% on improved pricing across consumer and merchant books. Operating expenses increased 50% YoY, reflecting stepped-up investment in free shipping, 1P, cross-border trade, and credit cards, which constrained operating leverage, with income from operations broadly in line with consensus and margins tightening sequentially versus 3Q25 after adjusting for one-offs. Adjusted free cash flow remained robust at quarter-end, underscoring resilient cash generation despite rapid credit growth.

Femsa posted positive 4Q25 results. Total revenues advanced 5.7% YoY (5.2% comparable), supported by positive trends across business units and a slightly favorable FX translation effect. Proximity Americas revenues rose 5.3% on a 4.4% SSS gain plus 4.6% store-base expansion. Proximity Europe revenues grew 2.5% (2.3% ex-FX), driven by stronger Swiss retail and some support from CHF appreciation. Health revenues rose 4.6% (6.7% currency-neutral) on resilience in Colombia and Ecuador despite Mexico headwinds and store rationalization. Fuel revenues increased 3.6% on an 8.7% same-station sales gain driven by 10.0% volume growth and a 1.2% lower price per liter plus higher wholesale volume. At the consolidated level, gross profit rose 0.5% but gross margin fell 220 bps to 41.5% due to mix and margin pressure in Coca-Cola FEMSA, Proximity Europe, Health, and Fuel (a 70-bps contraction on a comparable basis that excludes the cost reclassification). Adjusted EBITDA climbed 14.9% and margin expanded 150 bps to 18.1%. Consolidated net income jumped 33.6%, aided by below-the-line dynamics that included a non-cash FX loss versus a gain last year.

Coca-Cola FEMSA reported positive 4Q25 results. Consolidated revenues were up 2.9% YoY driven by revenue-growth-management initiatives and pricing, partially offset by unfavorable mix and FX translation, while volumes rose 1.3% YoY supported by South America and a mild decline in Mexico. Gross profit increased 1.8% YoY and the gross margin stood at 46.7%, reflecting pressure from mix and higher labor and depreciation costs, partly mitigated by lower sweetener and PET costs. EBITDA increased 12.8% YoY and the EBITDA margin reached 23.4%, benefiting from operating leverage and insurance recoveries in Brazil and Mexico, despite underlying cost pressures. Net profits advanced 3.0% YoY, supported by operating income growth and partly offset by higher financing costs and a higher effective tax rate.

Funo reported solid 4Q25 results. Total GLA grew 12.8% YoY driven by the consolidation of Fibra NEXT. Revenues rose 4.6% YoY supported by higher occupancy, inflation-linked rent increases and positive leasing spreads, with rental revenues increasing 4.3% YoY under similar drivers, partly offset by peso appreciation on USD-denominated leases. Consolidated occupancy remained resilient at 95.5%, broadly stable YoY. NOI was up 9.0% YoY supported by revenue growth and operating leverage, lifting the NOI margin by 310 bps YoY, while FFO increased 1.6% YoY with a slightly lower FFO margin due to higher financial expenses and FX effects. The quarterly distribution rose 21.5% YoY, underpinned by a near-full AFFO payout. LTV declined to 41.6% following the transfer of industrial assets and associated debt to the Fibra NEXT JV, strengthening the balance sheet.

Fibra Next reported solid 4Q25 results reflecting the consolidation of its industrial platform and strong operating execution. Total revenues reached MXN1.28 billion driven by higher stabilized GLA, contractual rent increases, and positive leasing spreads in both MXN- and USD-denominated contracts. EBITDA amounted to MXN1.027 billion supported by operating leverage and disciplined expense control, maintaining a high EBITDA margin. NOI amounted MXN$1.094 billion driven by revenue growth and stable property-level costs, resulting in a NOI margin close to 90%. FFO reached MXN$524.9 million supported by higher NOI and an expanded asset base, with a robust FFO margin. LTV remained conservative at 34.3%, reflecting a prudent capital structure and compliance with debt covenants. During the quarter, Fibra NEXT executed the joint venture with Fibra Uno, completed a bond exchange to optimize its USD debt profile, advanced strategic acquisitions including Doña Rosa II and the approved Triple Home Run portfolio, and strengthened its ESG positioning.

Televisa reported mixed 4Q25 results with lower revenues but expanding margins, exceeding expectations. Total revenues declined 4.5% YoY driven by a sharp 16.8% contraction in SKY revenues reflecting accelerated subscriber losses (-25.9%) due to structural video disconnections. Residential services revenues declined 0.6% YoY driven by ongoing video churn, largely offset by growth in broadband, mobile, and voice. Enterprise services revenues fell 4.2% YoY driven by tough comparisons and the timing of revenue recognition in large projects. Operating segment income grew 6.1% YoY driven by operating efficiencies, cost synergies from the Cable and SKY integration, and lower corporate expenses, resulting in a 410-bps margin expansion. Net losses narrowed driven by higher operating income and lower other expenses, partly offset by higher income taxes related to deferred tax asset write-offs. For 2026, management guided further margin expansion through efficiency gains, sustained growth in broadband and mobile, continued rationalization of the SKY business, and the suspension of dividends to preserve financial flexibility for potential telecom investment opportunities.

TelevisaUnivision reported weak 4Q25 results. Total revenues declined 2% YoY, reflecting weaker US trends offset by Mexico, which supported by favorable FX and ViX momentum; advertising revenues were flat YoY, as a double-digit decline in the US due to lower political advertising was fully offset by strong growth in Mexico driven by ViX and private-sector linear demand; subscription and licensing declined 4%, explained by the renewal cycle with a key Mexican distributor despite continued growth in the U.S. and ViX’s premium tier; other revenues fell 20% due to lower ancillary income. Adjusted OIBDA decreased 12% YoY, pressured by operating deleverage and higher expenses, while the adjusted OIBDA margin compressed to 29.9%. Net profits remained negative, though losses narrowed materially versus the prior year due to lower impairment charges and improved operating income.

Grupo Bimbo reported solid 4Q25 results. Total revenues declined 1.5% YoY in peso terms but increased 3.9% excluding FX, driven by favorable price/mix, market share gains, and contributions from recent acquisitions, while regional performance showed North America revenues down 11.3% YoY due to FX and soft consumption, Mexico revenues up 4.8% YoY supported by mix and volume growth across channels, EAA revenues up 13.9% YoY on strong QSR performance and double-digit growth in key markets, and Latin America revenues up 6.4% YoY reflecting broad-based local-currency growth and the Wickbold acquisition. Gross profit declined 2.8% YoY with gross margin contracting 70 bps to 51.8%, pressured by higher raw material, labor, and indirect costs, partially offset by pricing and productivity initiatives. EBITDA increased 14.3% YoY, with EBITDA margin expanding 200 bps to 14.7%, supported by record productivity gains in North America, strict cost control, and lower restructuring expenses. Net profits increased 1.2% YoY as higher operating performance offset higher financing costs.

Orbia reported neutral 4Q25 results. Total revenues increased 5% YoY, driven by higher volumes and improved mix in Connectivity Solutions, Fluor & Energy Materials, Building & Infrastructure, and Precision Agriculture, partially offset by weaker Polymer Solutions. EBITDA grew 2% YoY, supported by stronger performance in Fluor & Energy Materials, Building & Infrastructure, and Connectivity Solutions, while the EBITDA margin contracted 38 bps to 12.1% due to higher input costs and mix effects. The net loss widening 141% YoY, reflecting higher financial costs and a significantly higher tax expense despite stronger operating income. Free cash flow rose 64% YoY, explained by higher operating cash flow from efficient working capital management and lower capital expenditures. For 2026, Orbia expects an EBITDA between US$1.1–1.2 billion, Capex of approximately US$400 million, an effective tax rate of 27%–32% excluding discrete items, no ordinary dividend declaration, and continued positive momentum in Precision Agriculture, Fluor & Energy Materials, and Connectivity Solutions, while Polymer Solutions and Building & Infrastructure markets remain relatively weak. Orbia announced the appointment Cristian “Cape” Capellino as its new CFO effective March 15th, 2026, in substitution of James P. “Jim” Kelly, who will retire as CFO after four years of service. Mr. Capellino joined Orbia in 2020 and has held senior leadership roles across Controllership, Tax, Financial Planning and Analysis and most recently, Finance Transformation. Prior to Orbia, Capellino held senior finance and business leadership roles at Tenaris, a NYSE listed global industrial company. He holds an MBA from the MIT Sloan School of Management and a Public Accountant degree from the National University of Córdoba.

Pinfra delivered neutral 4Q25 results. Total revenues rose 10% YoY, supported by higher toll road traffic, a sharp acceleration in construction activity, and stronger asphalt mix sales, partly offset by the deconsolidation of the Altamira Port Terminal. EBITDA advanced 3% YoY, reflecting resilient concession performance and incremental contributions from construction and plants, while the EBITDA margin narrowed to 60% from 64% due to mix effects and lower operating leverage. Net profits fell 60% YoY, driven by an adverse comprehensive financial result related to a non-cash FX loss on US dollar exposure.

Gentera delivered solid 4Q25 results. Total loan portfolio expanding 13.1% YoY driven by strong growth at Banco Compartamos México, Compartamos Perú in local currency, and ConCrédito, while the NPL ratio improved 10 bps YoY to 3.83%, reflecting disciplined underwriting and stable asset quality. Net interest income increased 19.5% YoY supported by portfolio expansion and higher yields, with NIM widening 180 bps YoY to 42.2% as interest income growth outpaced funding costs amid easing reference rates. Provisions rose 22.9% YoY, consistent with accelerated portfolio growth and mix effects, leading adjusted net interest income to increase 18.1% YoY and NIM after provisions to expand 90 bps YoY to 29.5%. Net commissions advanced 16.4% YoY, fueled by strong insurance activity across subsidiaries, while operating expenses increased 11.2% YoY due to higher headcount, variable compensation, and strategic initiatives, partially offset by efficiency gains. Net income grew 6.4% YoY, supported by stronger operating income despite higher provisions and taxes, and ROE stood at 23.2%, down 40 bps YoY but remaining at a high level. During the quarter, the company proposed a new dividend policy with payouts of up to 45% of net income and reiterated 2026 guidance calling for loan portfolio growth of 13%–16% and EPS in the range of Ps. 5.88–6.03, implying 13%–16% YoY growth, underpinned by continued portfolio expansion, stable asset quality, and operating discipline.

Liverpool reported neutral 4Q25 results. Total revenues rose 5.0% YoY, with retail sales expanding 4.3% supported by Buen Fin traction, Liverpool same store sales increasing 3.3% and Suburbia advancing 0.5% in a highly promotional environment, financial gains climbing 13.6% on credit portfolio growth and higher card penetration, and real estate sales improving 6.7% driven by occupancy gains and lease renegotiations; the NPL ratio reached 3.7%, up 53 bps YoY, aligned with the stated risk strategy. EBITDA grew 3.0% YoY despite logistics and labor cost pressures, while EBITDA margin contracted 40 bps to 19.3%, and net profits declined 21.4% YoY reflecting higher provisions, Nordstrom-related PPA charges, and increased financial expenses. For 2026, management emphasized margin recovery as logistics normalization advances, prudent credit expansion with NPLs broadly stable, conservative leverage with net debt to EBITDA at 0.52x, and disciplined capex following the near completion of the Arco Norte logistics center. The company announced the creation of a new line of business after establishing an alliance with fashion brand giant Authentic Brands Group to exclusively distribute the Dockers brand in Mexico, as part of its diversification strategy.

Esentia posted solid 4Q25 results. Adjusted revenues increased 10.9% YoY driven by higher natural gas sales and capacity growth following the full consolidation of SLM. Adjusted EBITDA rose 5.7% YoY reflecting operating leverage despite higher transportation costs, and the EBITDA margin stood at 70%, versus 74% a year earlier due to cost reclassifications and IPO-related effects. Net income surged 284.7% YoY supported by lower net financial costs and the use of tax loss carryforwards. Net debt declined 26% YoY and the net debt to adjusted EBITDA ratio improved to 4.1x from 5.9x, underscoring balance sheet deleveraging. For 2026, management guided adjusted EBITDA in the range of approximately flat to low-single-digit growth versus 2025, supported by disciplined execution of Phase I of the expansion plan and sustained operational efficiency.

Becle reported weak 4Q25 results, despite resilient profitability. Revenues declined 14.1% YoY driven by an 8.8% YoY contraction in volumes reflecting distributor destocking in the US and Canada, softer consumption trends in Mexico, and negative FX translation, partly offset by RTD growth and expansion in the Rest of the World. Gross profit declined 12.4% YoY, while gross margin expanded 110 bps supported by lower agave-related input costs and sourcing efficiencies, despite peso appreciation. EBITDA was broadly flat YoY as the EBITDA margin expanded 340 bps driven by gross margin gains and other income related to U.S. distribution settlements. Net income fell 12.1% YoY mainly due to a higher effective tax rate despite improved financial results and FX gains.

Genomma Lab reported weak 4Q25 results. Total revenues declined 13.9% YoY driven by an intentional reduction in Mexico sell-in to normalize elevated retailer inventories, FX headwinds, and a softer consumption environment, while gross profit decreased 16.7% YoY reflecting lower volumes and unfavorable operating leverage. Gross margin contracted 210 bps YoY to 61.0% due to the sharp decline in Mexico sell-in and fixed-cost absorption pressures, partially offset by cost containment initiatives. EBITDA declined 16.5% YoY, with the EBITDA margin compressing 70 bps to 22.1%, as productivity savings and lower SG&A only partially mitigated operational deleverage. Net income from continuing operations decreased 13.0% YoY, mainly explained by lower operating income and higher effective tax expense despite lower net financing costs and reduced FX losses.

Grupo Elektra reported large net losses in 4Q25 after reaching a settlement on fiscal disputes. Consolidated revenues increased 2% YoY driven by a 9% YoY expansion in financial income reflecting strong loan portfolio growth at Banco Azteca, partially offset by an 8% YoY decline in commercial sales due to softer retail demand. Operating costs and expenses declined 1% YoY driven by a 13% reduction in commercial costs from margin-focused retail strategies, partly offset by a 20% increase in financial costs due to higher loan loss provisions. EBITDA grew 5% YoY driven by revenue growth and lower commercial costs, while the EBITDA margin remained broadly stable. Net losses widened to MXN$19.9 billion driven by a large income tax provision related to the settlement of all outstanding tax litigation with the Mexican government.

Asur reported weak 4Q25 results. Total operating revenues advanced 21.6% YoY, driven by a sharp increase in construction revenues and stable aeronautical and non-aeronautical revenues excluding construction. Total passenger traffic increased 0.9% YoY, reflecting resilient demand despite mixed regional trends. Mexico traffic was up 0.1% YoY, supported by international traffic growth that offset weaker domestic volumes. San Juan traffic declined 3.1% YoY, pressured by softer domestic demand despite higher international flows. Colombia traffic rose 5.7% YoY, driven by strong international and domestic passenger growth. EBITDA declined 4.8% YoY due to higher operating costs, increased depreciation in Colombia from the concession amortization method change, and the dilution effect of construction revenues, while the EBITDA margin compressed to 44.4% from 56.7%. Net profits fell 21.9% YoY, reflecting lower operating income, foreign exchange losses, and higher financial expenses.

Gap delivered neutral 4Q25 results. Total revenues advanced 2.8% YoY, supported by a 12.6% rise in aeronautical revenues reflecting higher regulated airport fees in Mexico and new routes, and a 13.3% increase in non-aeronautical revenues driven by stronger commercial activity and the cargo and bonded warehouse business. Passenger traffic declined 0.9% YoY due to hurricane-related disruptions in Jamaica, which offset resilient demand trends in Mexico. EBITDA grew 7.5% YoY on operating leverage in Mexico and cost discipline, although the EBITDA margin narrowed to 51.7%, from 49.4%, amid higher maintenance, personnel and service expenses. Net profits declined 17.4% YoY, mainly due to higher financial expenses, negative FX translation effects and a higher tax charge. The 2026 guidance, which excludes CBX consolidation, calls for passenger traffic growth of 2%–5%, aeronautical revenue rising 9%–12%, non-aeronautical revenue increasing 6%–9%, total revenue up 8%–11%, EBITDA growth of 8%–11%, an EBITDA margin of 65% ±1%, and MXN$13.5 billion Capex, underpinned by regulated tariff application, commercial income expansion and gradual traffic normalization in Jamaica.

Oma reported positive 4Q25 results. Total revenues were flat YoY due to lower construction revenues offsetting a 6.1% increase in regulated and commercial revenues, driven by higher passenger traffic and stronger commercial activity. Aeronautic revenues rose 5.6% YoY supported by a 6.0% increase in total passenger traffic and higher domestic volumes, while non-aeronautic revenues advanced 7.5% YoY reflecting higher parking, restaurants, retail and VIP lounge penetration. Adjusted EBITDA increased 5.9% YoY due to operating leverage and revenue mix, while the adjusted EBITDA margin edged down YoY reflecting higher maintenance provisions and concession taxes. Net profits grew 3.6% YoY, supported by lower financing expenses despite higher operating costs.

Volaris reported neutral 4Q25 results. Total operating revenues were up 5.6% YoY, driven by higher ASMs (+5.6%) and a 6.1% increase in ancillary revenues per passenger, while the load factor declined 2.2 PP to 85.1%. Total operating expenses rose 8.9% YoY, reflecting higher fuel prices, maintenance, and airport-related costs, which pressured profitability. EBITDAR was down 0.9% YoY and the EBITDAR margin contracted 2.4 pp to 37.2%, despite disciplined cost control and a stable CASM ex-fuel profile. Net profits fell 91.3% YoY, affected by higher taxes and cost inflation, while net debt to LTM EBITDAR increased to 3.1x from 2.6x. For 2026, management guided for ASM growth of approximately 7%, an EBITDAR margin around 33%, capex of about US$350 million, and average fuel prices of US$2.10–2.20 per gallon, with 1Q26 EBITDAR margin expected near 25% amid temporary cost pressures related to GTF engine inspections.

Alsea posted neutral 4Q25 results. Total revenues advanced 0.5% YoY driven by sequential improvement in Mexico, resilient performance in Spain, and a recovery in South America, partially offset by FX headwinds, while same store sales increased 3.3% YoY supported by traffic recovery, value propositions, and operational execution across formats. The company opened 169 units during 2025, with total stores increasing marginally YoY, reflecting a disciplined expansion strategy focused on returns, while digital sales grew 13.4% YoY and reached 39.6% of total sales, supported by stronger delivery capabilities, aggregators, and loyalty integration. Active users in loyalty programs reached 8.2 million, reflecting higher engagement and improved omnichannel execution. EBITDA excluding IFRS 16 increased 2.9% YoY, with the EBITDA margin expanding 40 bps YoY to 16.8%, driven by productivity initiatives, labor efficiencies, and portfolio mix improvements. Net profits increased 32.0% YoY, supported by higher operating leverage and lower extraordinary items, while net debt to EBITDA declined to 2.4x, reflecting improved cash generation and disciplined capital allocation.

Grupo Chedraui reported neutral 4Q25 results. Total revenues were down 3.0% YoY, driven by a decline in U.S. sales amid weaker traffic and a negative FX translation effect from a 10% peso appreciation, partially offset by solid Mexico performance. Mexico same store sales increased 3.0% YoY, supported by a higher average ticket and marginally higher transactions, while US same store sales declined 2.8% YoY in USD due to stricter immigration enforcement and SNAP disruptions. Gross profit rose 2.9% YoY and gross margin expanded 133 bps to 23.2%, reflecting more efficient promotions and inventory management in Mexico and initial efficiencies from the Rancho Cucamonga distribution center in the US. EBITDA declined 2.2% YoY, although the EBITDA margin improved 7 bps to 7.7%, as operating leverage gains and margin expansion were offset by additional non-recurring expenses in Mexico related to a revision by fiscal authorities and higher provisions in the US. Adjusted EBITDA excluding additional expenses grew by 9.7%, and the EBITDA margin of 8.6% was 101 bps higher than the same quarter of the previous year. Net profits increased 0.1% YoY, remaining broadly flat due to higher operating expenses and financial costs despite stronger gross profitability.

La Comer delivered solid 4Q25 results. Total revenues increased 9.5% YoY driven by positive price mix, strong performance across all formats, and higher traffic, while same store sales rose 6.4% YoY supported by promotional campaigns, strength in perishables and prepared foods, and solid regional execution, particularly in the North. Gross profit increased 11.3% YoY, with gross margin expanding 51 bps YoY to 30.5% due to favorable product mix and continued efficiencies in distribution and inventory management. EBITDA grew 18.4% YoY, and the EBITDA margin expanded 67 bps YoY to 8.9%, reflecting operating leverage, disciplined expense control, and the absence of extraordinary costs recorded in 4Q24. Net profits increased 24.1% YoY, supported by higher operating income and stable financing results despite higher taxes.

Soriana delivered weak 4Q25 results. Total revenues were down 2.9% YoY due to an unfavorable comparison base from extraordinary income in 4Q24, while same store sales declined 2.6% YoY reflecting eaker traffic and a challenging consumption backdrop. Gross margin expanded 100 bps to 24.8%, supported by improved commercial conditions and tighter markdown management, which allowed gross profit to increase 1.1% YoY despite lower sales. EBITDA fell 9.4% YoY and the EBITDA margin compressed to 7.4%, driven by higher operating expenses mainly associated with personnel costs following the minimum wage increase and the net addition of new stores, partially mitigated by an expense control plan implemented during the year. Net profits fell 29.6% YoY, explained by lower operating income despite a meaningful reduction in net financial cost.

Fibra Danhos reported positive 4Q25 results. Total portfolio GLA expanded 14.7% YoY driven by the delivery of industrial developments, while average occupancy increased 220 bps YoY supported by full industrial occupancy and resilient retail performance. Total revenues rose 6.5% YoY reflecting incremental industrial cash flow contributions and higher parking and ancillary revenues. NOI increased 6.5% driven by higher leased area in industrial assets, stable rental rates in retail properties, and lower rent losses, partially offset by FX effects in the office segment; the NOI margin remained broadly stable YoY underpinned by disciplined cost control. FFO advanced 9.0% YoY supported by higher NOI and scale effects, with the FFO margin improving modestly as operating leverage offset higher interest expense.

Nemak reported weak 4Q25 results. Total revenues increased by 1.2% YoY, supported by higher volumes and aluminum prices despite a high comparison base from one-time commercial negotiations in 4Q24. Volume increased 1.9% YoY, reflecting relatively resilient customer production schedules amid softer global auto demand and slower EV adoption. EBITDA declined 24.6% YoY, pressured by impairment charges, extraordinary operating expenses in North America, currency effects, and the absence of prior-year one-off commercial benefits. The EBITDA margin compressed to 10% from 13%, driven by lower profitability in North America, partially offset by solid operating efficiencies and margin expansion in Europe and Rest of the World. Net income posted a wider YoY loss, mainly due to impairments and foreign exchange losses, which more than offset lower financial expenses and taxes. For 2026, the company expects revenues of US$5.3-5.5 billion, EBITDA of US$630-650 million and Capex of US$385-395 million.

Traxión reported neutral 4Q25 results. Total revenues rose 45.7% YoY, driven mainly by a 143.6% increase in Logistics and Technology, as a result of the Solística acquisition and a large-scale project in the pharmaceutical sector. Mobility of People sales advanced 6.6% supported by the efficiency and customer profitability plan which boosted the revenue per kilometer. However, Mobility of Cargo revenues fell 22.4% due to lower demand and pricing pressure as a result of tariff uncertainty and the FX impact. Total costs and expenses grew 61.3% YoY due to a 124.7% increase in facilities, services and supplies deriving from the Solística incorporation. This led to a 0.3% YoY decrease in consolidated EBITDA, while the EBITDA margin contracted 580 bps to 12.6%. Net income was down 18.0% YoY due to higher depreciation. Operating cash flow more than doubled, while Capex was significantly lower, in line with the strategy of maintaining a solid balance sheet and high free cash flow generation. The net debt to EBITDA ratio closed at 2.2x, in line with the pre-Solística acquisition level.

Vinte delivered positive 4Q25 results. Revenues increased 13.5% on a proforma basis, primarily driven by higher average prices (+15.7%) that offset a slight 0.6% decline in volume. Gross and EBITDA profitability improved due to synergies with Javer, mainly in material procurement. This allowed gross profit to increase by 19.8% and EBITDA to grow by 27.1%. Net income rose by 23.5% due to favorable operating performance that offset a larger tax reserve. Vinte closed the quarter with leverage of 2.58 times, the lowest level since 2019, due to its strong free cash flow generation.

Promotora de Hoteles Norte 19 reported soft 4Q25 results. Total revenues rose 4.3% YoY, driven by higher ADR and portfolio optimization despite a slight contraction in rooms, while ADR increased 1.5%, occupancy stood at 56.8% with a marginal YoY decline, and RevPAR advanced 1.4% supported by rate discipline and stable demand. Adjusted EBITDA declined 4.9% YoY due to higher payroll costs and restructuring expenses, with the adjusted EBITDA margin compressing 220 bps to 22.3%, while EBITDA fell 5.7% and the EBITDA margin decreased 230 bps to 22.0% reflecting operating deleverage. He company reported a MXN$34.6 million net loss versus last year’s MXN$59.8 million net profit, mainly explained by extraordinary losses and the sale of the SLP property in 4Q24.

Actinver reported positive results for the year despite lower net profits in 4Q25. Total operating revenues were up 17% YoY in the quarter, mainly due to a strong performance across all business lines. The financial margin increased 9% due to lower interest rates that helped improve the funding cost, resulting in an 18% reduction in interest paid even though traditional deposits were 15% higher. In addition, provisions decreased 59%, boosting the adjusted financial margin by 22%. Net fees and commissions rose 24% given the significant growth of assets under management, investment banking, fiduciary services and transactional activity. Trading gains increased 22% due to market volatility and higher money market and FX revenues. However, this was partially offset by a 25% rise in administrative expenses given the 7% expansion of the workforce, higher variable compensation and the digitalization process. This led to a 12% drop in quarterly net income to MXN$429 million. The L12M ROE stood at 17.87%, compared to 15.25% in 4Q24.

Fibra Storage posted favorable 4Q25 results. Total revenues advanced 17.9% YoY, primarily driven by a 10.3% increase in leased GLA, given a 174 bps improvement in occupancy to 83.5% (the highest since 3Q023) and net absorption of 4,558 sq m (with a sequential 0.4 PP expansion in the move-in/move-out spread), and a 7.0% rise in average monthly rate (+7.6% same-store). Additionally, the average stay extended by 2.1 months to 30.3 months. Monthly RevPAM increased 9.3% to MXN$329.3, a historically high level, reflecting the favorable combination of higher rates and portfolio utilization. This strong revenue performance, combined with operating leverage, generated higher profitability. NOI rose 19.2%, with a margin expansion of 90 bps to 78.0%. EBITDA grew 21.5%, while the EBITDA margin improved 170 basis points to 57.7%. Adjusted FFO AMEFIBRA was up 20.6%.

Médica Sur registered strong 4Q25 results. Revenues increased by 8.0% YoY, driven primarily by higher demand for hospital services. EBITDA grew 13.3% YoY, while EBITDA margin expanded 100 bps to 21.6%, reflecting operating leverage and a more profitable services mix. Net income rose 2.6% YoY to MXN$139 million (vs. MXN$134 million estimated), as the strong operating performance was partially offset by an FX loss and a higher tax burden.

Grupo Sports World delivered weak 4Q25 results. Total revenues rose 12.6% YoY, driven by price normalization, stable active customers, higher corporate health plans, sponsorships, exchanges, and stronger in-club activity. Active customers edged down 0.5% YoY, reflecting a deliberate profitability-focused strategy centered on higher-value clients. The number of gyms remained stable at 48 operating clubs, with one additional club in a pre-operational stage. EBITDA under IFRS 16 declined 23.6% YoY, explained by a sharp increase in depreciation from lease accounting effects, while the EBITDA margin closed at 36.5%, down YoY due to the same IFRS 16 dynamics. The net loss under IFRS 16 narrowed to MXN$6.4 million, from last year’s MXN$180.2 million, due to an adjustment in the tax rate generated by the reduction in deferred taxes.

Cemex has reached an agreement to acquire all assets of Omega Products International, a leading manufacturer of stucco in the western United States. Omega generates approximately US$23 million in EBITDA per year. The transaction currently meets Cemex’s return and free cash flow conversion criteria, with an expected post-synergy multiple below 7x. This operation continues to reinforce Cemex’s commitment to disciplined capital allocation and long-term shareholder value, while supporting its strategy to expand U.S. operations and diversify into high-growth performance materials. The transaction is expected to close during the first quarter of 2026.

Sigma Foods placed MXN$10 billion in domestic debt securities in two tranches: i) SIGMA 26 for MXN$3.45 billion, with a 5-year term, at a variable rate of TIIE Funding + 0.53%; ii) SIGMA 26-2 for MXN$6.55 billion, with a 10-year term, at a fixed rate of 9.17%, equivalent to a spread of +0.49% with respect to the benchmark M Bond rate. Both tranches received ‘AAA(mex)’ from Fitch Ratings and ‘AAA.mx’ from Moody’s Local, with a stable outlook.

GCC announced the acquisition of three companies and their aggregates, asphalt, and ready-mix concrete operations in El Paso, Texas. This transaction strengthens GCC’s growth strategy by incorporating a platform with approximately US$30 million in annual revenues and reinforcing its operational presence in the El Paso, Texas region. In addition, the deal includes aggregate reserves with an estimated useful life of around 50 years, supporting long-term supply in that market. The transaction is expected to generate operational synergies and contribute positively to GCC’s cash flow generation profile starting in 2026.

Fibra Mty, has executed an agreement to sell aportfolio comprising five properties for US$46.8 millon plus applicable VAT including: four office buildings and one retail property located in Monterrey, San Luis Potosi, and Ciudad Juarez. The transaction is part of the Trust’s initiatives to optimize its investment property portfolio. Net proceeds from the sale may be used to fund investments in industrial properties and/or the operate Fibra Mty’s CBFI buyback program.

TV Azteca’s owners have decided to file for a voluntary “Concurso Mercantil” proceeding (Mexican version of Chapter 11) in the coming days, a process that will allow the company to reorganize its liabilities while suspending any judicial enforcement actions and maintaining ongoing operations, according to local newswires.

OTRAS EMPRESAS

The National Antitrust Commission rejected Visa’s acquisition of a 51% equity stake in Prosa after concluding that the transaction would eliminate a direct competitor in card payment processing and create risks for users of the financial system.

ECONÓMICO

4Q25 GDP was revised upwards to +0.9% QoQ, from an original level of 0.8%, which was the best performance in the last 5 quarters, INEGI reported. Both secondary and tertiary activities grew 0.9%, while primary activities were down 1.4%. As a result, 4Q25 GDP was up 1.8% YoY and 2025 GDP rose 0.6% based on original data.

The headline inflation rate was 0.25% in the first half of February, above the 0.18% consensus forecast of the latest Citi Mexico expectations survey. The core inflation rate increased 0.22%, below the 0.26% consensus projection, with merchandise and services broadly contributing to underlying pressures. The bi-weekly non-core inflation rate rose 0.32%, primarily driven by higher prices for fruits and vegetables and partially offset by lower energy and regulated tariffs. On an annual basis, headline inflation accelerated to 3.92%, the highest level since June 2025, while the core inflation rate reached 4.52%, the highest since March 2024.

The IGAE increased 0.4% MoM (seasonally adjusted) in December 2025, marginally stronger than the 0.2% consensus forecast, INEGI reported. Primary activities expanded sharply by 6.5%, while secondary and tertiary activities advanced modestly by 0.2% each. The IGAE rose 3.3% YoY (original data) in December 2025, achieving the best performance since July 2024 and outperforming market forecasts of 2.6%. Primary activities were up11.4%, secondary activities grew 2.4% and tertiary activities increased 3.2%.

Foreign investment increased 7.7% to a record level of US$40.9 billion in 2025, according to the Economy Ministry. Reinvestments were down 3.7% to US$27.65 billion, new investments increased 132.9% to US$7.4 billion and intercompany transactions 17.0% to US$5.8 billion. The US remained the largest foreign investor in Mexico with 38.8% of total, followed by Spain with 10.8%, Canada with 8.1%, Netherlands with 5.8% and Japan with 5.6% and others with 30.9%.

Service sector’s revenues fell by 0.7% MoM (seasonally adjusted) in December 2025, reversing the 0.7% MoM increase of the previous month, according to INEGI. However, service sector’s revenues were up 1.1% YoY (original data).

Retail sales declined by 0.1% MoM (seasonally adjusted) in December 2025, according to INEGI. However, retail sales were up 4.3% YoY (original data).

Construction output increased 1.7% MoM (seasonally adjusted) in December, which was the third month in a row with a positive performance, INEGI reported. However, construction output fell 4.9% YoY based on original data.

The trade balance registered a US$6.5 billion deficit in January, according to INEGI. Total exports rose 8.1% YoY to US$48.0 billion (oil -33.5%; non-oil +9.8%), while imports increased 9.8% to US$54.5 billion (oil -21.3%, non-oil +12.7%).

Unemployment reached 2.7% in January 2026, in line with the January 2025 level, according to INEGI.

Hacienda executed a MXN$175.6 billion refinancing operation aimed at optimizing the domestic debt maturity profile and improving local market liquidity. The transaction replaced Cetes, M Bonds, and Udibonos maturing between 2026 and 2050 with similar instruments maturing between 2027 and 2057, extending the average maturity by 6.62 years. The operation aligns with the 2026 Annual Financing Plan and reflects a proactive liability management strategy.

Economists continue expecting a 25-bps cut in Banco de Mexico’s key interest rate at the May meeting, unchanged versus the previous survey, according to the latest Citi Mexico expectations survey. The policy rate forecast for YE26 and YE27 stayed at 6.5%. GDP growth expectations were stable, with the median forecast for 2026 unchanged at 1.4% and the 2027 estimate also holding at 1.8%. Headline inflation expectations for YE26 remained at 4.0%, while core inflation edged up to 4.15%, from 4.10% previously; for YE27, headline inflation increased slightly to 3.75%, from 3.73% and core inflation rose to 3.74%, from 3.71%. Peso expectations strengthened, with the USDMXN projection improving to 18.20 for YE26 from 18.35, and to 18.76 for YE27 from 19.00.

Congress approved the constitutional reform to gradually reduce workweek hours from 48 to 40 by 2030. The reform was turned over to the 32 state congresses. Once this process concludes, the reform will be submitted to the Executive Branch for final promulgation.

Subasta CETES: 28-day CETES -1 bps to 6.83%; 91-day CETES +10 bps to 7.05%; 175-day CETES -6 bps to 7.05% and 721-day CETES -4 bps to 7.54.

Descargar PDF: Mexican Market Chatter Febrero 20 – Febrero 27