MERCADOS

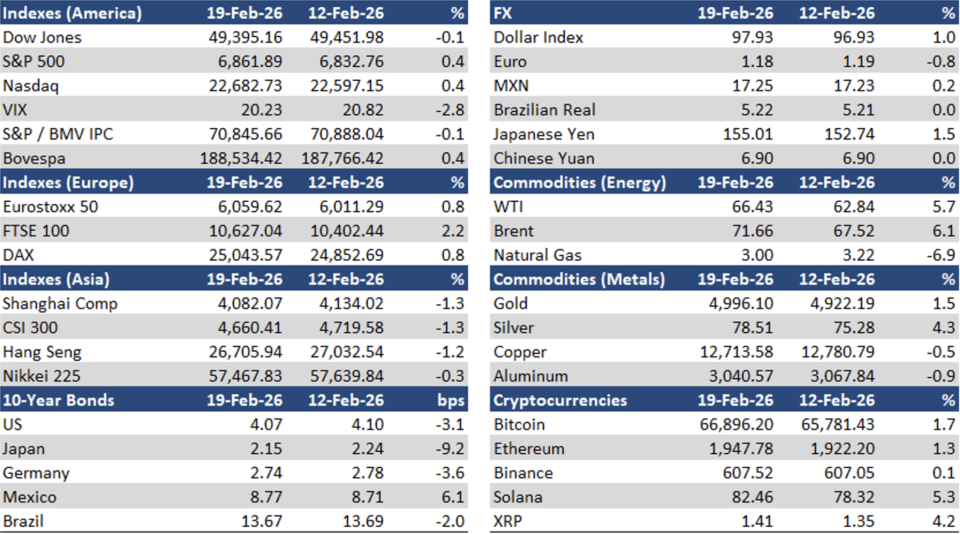

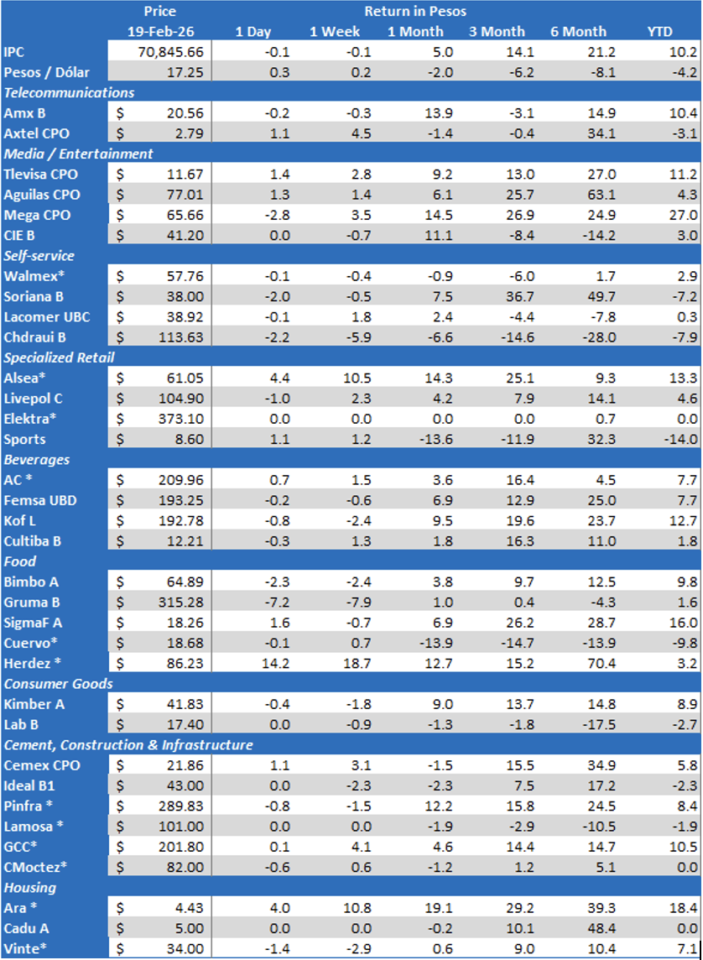

En S&P / BMV IPC experienced some marginal profit taking (-0.1%) after last week’s rally, amid mixed quarterly results. Meanwhile, the Mexican peso lost 0.2% to close at MXN$17.25/USD; the yield of the 10-year M-Bono was up 6 bps to 8.77%.

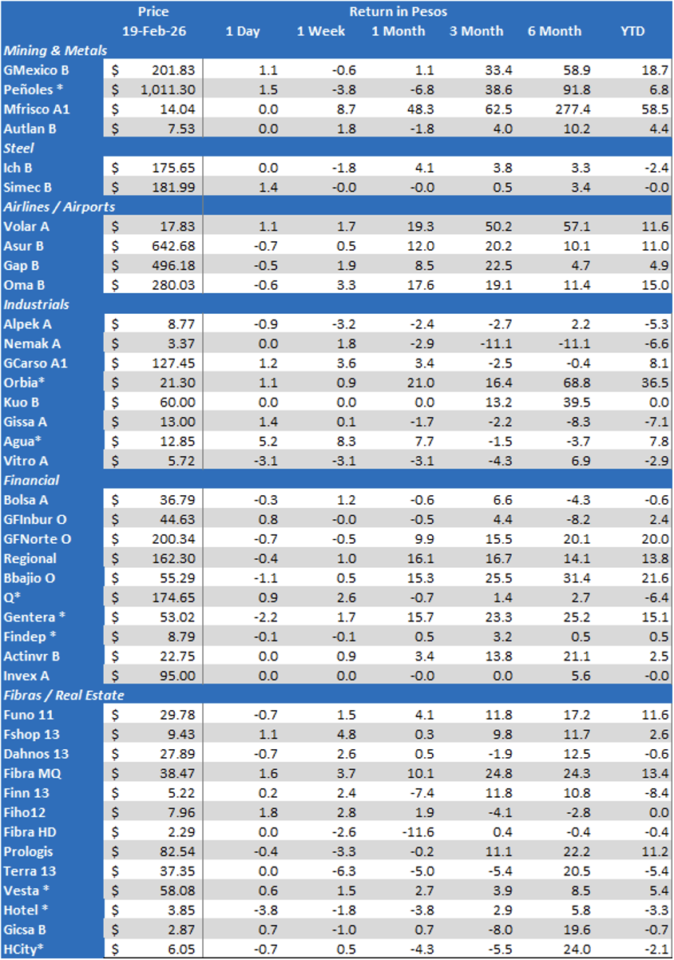

En S&P / BMV IPC's top gainers were: ALSEA * (+10.5%), GCARSO A1 (+3.6%), and OMA B (+3.3%). On the other hand, the main losers were: GRUMA B (-7.9%), PEÑOLES * (-3.8%) and KOF UBL (-2.4%).

EMPRESAS COTIZADAS

Walmex delivered soft 4Q25 results. Consolidated revenues were up 3.0% YoY (Mexico +4.9%, Central America +2.4% in constant currency), supported by new store contribution (1.7% of growth), continued EDLP execution, and improved availability. Same-store sales in Mexico increased 3.3% (ticket +3.9%, traffic -0.5%) and showed a modest sequential deceleration versus 3Q25, while Central America SSS rose 0.6% (ticket +1.5%, traffic -0.8%) amid softer consumption and competitive pressure, particularly in Costa Rica. E-commerce remained a structural tailwind, with Mexico eCommerce GMV up 13.3% YoY (On-Demand +19.1%, Marketplace +15.3%) and penetration at 9.1% of total GMV, while Central America eCommerce GMV rose 34% YoY. Gross margin expanded 30 bps YoY to 24.0%, reflecting commercial margin improvement and higher contribution from new businesses; gross profit advanced 4.6% YoY. EBITDA grew 8.1% YoY and EBITDA margin widened 50 bps to 10.5%, as SG&A held flat at 15.9% of sales on operating efficiencies and a one-off benefit that offset growth investments. Net profit declined 3.9% YoY and net margin compressed to 5.2%, primarily due to a higher effective tax rate. The company will reduce 30% of SKU’s in its Bodega Aurrerá and Mi Bodega to compete with Tiendas 3B and Tiendas Bara.

Gruma reported soft 4Q25 results. Total revenues increased by 2% YoY driven by strength in Europe, Asia & Oceania, and Central America offsetting softer US food service trends. Volumes were flat YoY, reflecting resilient demand outside the U.S., while gross profit declined 1% and gross margin contracted 140 bp due to higher raw material and logistics costs, resulting in a slight miss versus consensus expectations. EBITDA fell 5% with a 130 bp margin contraction, as cost pressures outweighed pricing and mix benefits. Net profit decreased 18% YoY, mainly due to lower operating income and adverse FX effects.

Sigma Foods announced the following appointments, effective as of February 13, 2026: Álvaro Fernández retains his current position as Chairman of the Board of Directors of Sigma Foods; Rodrigo Fernández, CEO of Sigma Alimentos, S.A. de C.V., has been appointed CEO of Sigma Foods; Roberto Olivares, CFO of Sigma Alimentos, S.A. de C.V., has been appointed CFO of Sigma Foods; and, Carlos Argüelles has been appointed General Counsel of Sigma Foods.

Fibra Macquarie reported neutral 4Q25 results. Total portfolio GLA expanded 0.6% YoY to 36.6 million square feet, driven by incremental industrial additions and acquisitions, while average occupancy declined 136 bps YoY to 94.9% reflecting portfolio rotation and stabilization dynamics. Revenues decreased 0.6% YoY, explained by FX effects and lower average occupancy, while Net Operating Income including SLR fell 2.1% YoY due to margin compression and higher property-level costs, resulting in a 131 bps YoY contraction in the NOI margin including SLR. FFO declined 9.4% YoY and the FFO margin compressed 482 bps YoY, reflecting higher financing costs and lower operating leverage, while LTV increased 44 bps YoY to 33.0%, remaining within conservative levels. For 2026, management guided AFFO per certificate of MXN$2.60–2.70, implying low single-digit growth in USD terms, with same-store performance expected to remain stable, industrial renewal spreads projected at 10–15%, cash distributions guided at MXN$2.45 per certificate. On the other hand, Fibra Macquarie acquired a 124-hectare industrial land parcel along Tijuana’s Boulevard 2000 submarket, for US$113.8 million, excluding transaction costs and taxes. Fibra Macquarie expects the project to achieve a stabilized yield on cost within a target 9%-11% range. The acquisition agreements incorporate a structured payment plan over three years from the transaction’s closing, with an initial cash payment of US$19.9 million on February 19th, with subsequent cash payments of US$19.9 million in the following months, US$39.8 million in February 2027 and US$34.1 million in February 2028 (all payments exclude transaction costs and taxes).

Aeromexico delivered solid 4Q25 results. Total revenues increased 0.2% YoY on a reported basis and 3.4% YoY on a normalized basis, driven by higher TRASM, an improved premium mix, and favorable FX. Total passengers declined 1.3% YoY to 6.2 million and ASMs decreased 1.8% YoY reflecting disciplined capacity management. Adjusted EBITDAR grew 12.5% YoY and the Adjusted EBITDAR margin expanded 3.8 PP to 35%, supported by pricing strength, operating discipline, and the extraordinary gain from the TechOps divestment. Excluding the TechOps transaction and IPO-related expenses, adjusted EBITDAR rose 8.3% YoY with the margin improving 1.4 PP to 30.2%. Net profits surged 119.0% YoY, reflecting stronger operating income and lower net financing costs. For 2026, management guided to ASM growth of approximately 3–5% YoY, total revenue growth of 7.5–9.5% YoY, an adjusted EBITDAR margin of 28.5–30.5%, an operating margin of 15–17%, and a reduction in adjusted net leverage toward ~1.6x.

Corporación Inmobiliaria Vesta reported positive 4Q25 results. Total rental income was up 17.2% YoY driven by new revenue-generating leases, inflation-linked rent escalations, higher straight-line IFRS adjustments, and incremental energy income. Adjusted NOI increased 17.1% YoY, supported by higher rental income and stable property costs relative to revenues, which expanded margins. Adjusted EBITDA rose 18.2% YoY, reflecting strong top-line growth and tighter administrative expense discipline as a share of revenues. Vesta FFO (-Tax Expense) declined 91.4% YoY due to a significantly higher current tax expense associated with Mexican peso appreciation, despite relatively stable pre-tax FFO. For 2026, management guided to rental revenue growth of 10.0–11.0%, an adjusted NOI margin of approximately 93.5%, and an adjusted EBITDA margin of around 83%, underscoring continued operating strength amid a normalized margin profile.

Megacable delivered solid 4Q25 results. Total revenues were up 8.2% YoY driven by double-digit Mass Segment growth supported by subscriber expansion and higher contribution from new territories, while Corporate revenues declined. Total RGUs increased 7.5% YoY reflecting sustained net additions across Internet, video and telephony, while ARPU remained flat YoY following the methodological change based on Internet subscribers. EBITDA rose 15.3% YoY due to operating leverage, cost discipline and efficiency initiatives, lifting the EBITDA margin to 44.0% from 41.3%. Net profits surged 74.2% YoY supported by stronger operating performance and an improved net financing result amid lower interest expenses and FX gains.

Bafar reported positive 4Q25 results. Consolidated revenues were up 14.7% YoY, driven by an 11.2% growth in food sales, explained by new store openings, the maturation of the retail channel, and a greater focus on value-added products. Fibra Nova revenues increased 14.8% YoY, supported by new contracts, continued portfolio expansion, and adjustments to dollar-denominated rents. Real estate sales rose 243.9% YoY following the launch of high-value developments, while agribusiness revenues fell 63.7% YoY due to the absence of walnut sales during the quarter. Gross profit advanced 10.3%, although the gross margin contracted 110 basis points to 28.2% due to higher raw material costs. Operating expenses decreased as a proportion of revenue, reflecting operational efficiencies and the revaluation of properties in the real estate division. As a result, EBITDA grew 22.4% YoY and the margin expanded 130 basis points to 20.6%. Net income registered a significant 136.5% YoY rise, supported by higher operating profits and FX gains.

Grupo Herdez reported solid 4Q25 results. Net sales were up 9.3% YoY driven by Preserves (mayonnaise, vegetables, spices and mole), Impulse (multipack and take-home Helados Nestlé with higher average ticket), and Exports (higher volumes of salsas and vegetables), while volumes rose 4.8% supported by wholesale and price clubs. Gross profit increased 13.0% with a 130-bps gross margin improvement on favorable mix in Preserves and FX and input relief in Exports, partially offset by cocoa cost pressure and channel mix in Impulse. EBITDA grew 13.0% with a 60-bps margin expansion as Preserves and Exports more than compensated Impulse softness. Net income increased 20.1% supported by operating leverage and a strong equity contribution from MegaMex following operational improvements in Don Miguel and guacamole. In 2026, the company expects a 7-9% revenue growth with operating cash flow between MXN$2.5-2.7 billion. Herdez will propose the payment of a MXN$15.0/share cash dividend (19.9% yield) at its March 6th ordinary shareholders’ meeting.

Invex Controladora reported neutral 4Q25 results. Consolidated net profits were down 24% YoY, reflecting lower trading gains despite solid operating execution across core businesses. Financial services revenues were up 13% YoY, driven by credit portfolio expansion and higher yields in money markets and derivatives but the pre-tax profits declined 44% due to lower trading gains. Energy Transition revenues rose 21% YoY, supported by a 28% YoY increase in electricity supply, a positive contribution from Texas operations. Pre-tax profits advanced 53% due to higher supply margins and the sale of clean energy certificates. Investment Promotion received distributions amounting to MXN$143 million. Invex Controladora closed the sale of its remaining 20% stake in GANA on February 12, after fulfilling regulatory requirements and obtaining third-party consents. Invex received CBFEs from FMX23 amounting to around MXN$3.96 billion, increasing its equity stake from 17.7% to 27.7%. The transaction was carried out in parallel with FMX23’s MXN$10.28 billion follow-on, including Invex’s stake. As a result, Invex expects to generate a MXN$1.2 billion extraordinary gain 1Q26. It will now recognize its share of FMX23’s profits using the equity method, given that it has acquired a significant influence.

Grupo Hotelero Santa Fé reported soft 4Q25 results. Total revenue was up 1.4% mainly due to a 2.6% increase in room revenue, a 1.1% rise in food and beverages and a 3.0% growth in third party hotel management fees. This was partially offset by a 2.0% fall in other hotel revenue and a 13.7% decrease in vacation club revenue. EBITDA was down 12.6% reflecting higher costs and expenses driven by inflation. The company reported a MXN$122.0 million net loss, reversing last year’s P$17.2 million net profit mainly due to other non-recurring expenses.

Fmty reported mixed 4Q25 operating results. GLA increased 9.6% YoY driven by industrial acquisitions and expansions, while total revenues rose 7.2% supported by the incorporation of the MeLi León and remaining Batach assets and higher leased area. NOI advanced 8.7% reflecting portfolio growth, and the NOI margin expanded 120 bps to 92.4% due to operating leverage and cost discipline. FFO declined 8.4% as a result of lower financial income following cash deployment into acquisitions and a lower benchmark rate, leading to a 12.9 PP contraction in the FFO margin to 75.4%.

Fibra Hotel posted weak 4Q25 results. Total revenues declined 5.4% YoY due mainly to a 324-bps reduction in occupancy levels due to softer demand, which was partially offset by a 5.5% ADR increase reflecting pricing discipline across regions. RevPAR rose 0.1% as higher ADR offset lower occupancy. Lodging contribution decreased 15.4% due to operating deleveraging and higher labor costs. For the same reason, EBITDA declined 19.1%, while the EBITDA margin contracted to 23.3%. FFO fell 18.0% following lower operating cash generation. AFFO was down 26.4% due to weaker EBITDA and higher cash outflows.

Consorcio Ara delivered a strong 4Q25. Revenues rose 30.5% YoY driven by a 25.8% increase in units sold and a 4.4% higher average price, reflecting robust demand in the middle-income and residential segments. Gross margin expanded 30 bp YoY to 26.2%, lifting gross profit by 32.0%. EBITDA advanced 25.8% YoY with an EBITDA margin of 13.2%, slightly lower YoY due to higher commercial and administrative expenses. Net profits surged 93.3% YoY supported by operating leverage and a favorable tax effect. For 2026, management expects to replicate the revenue growth achieved in 2025, underpinned by stable macro conditions, continued support from Infonavit, Fovissste, and private banks, and sustained demand across its core housing segments.

Cemex issued MXN$5.5 billion in long-term local bonds on February 19th. The five-year notes carry a floating annual interest rate of funding TIIE plus 70 bp and are guaranteed by Cemex Concretos, Cemex Operaciones México, Cemex Corp., and Cemex Innovation Holding. The company will use net proceeds for general corporate purposes, including but not limited, to debt repayment.

Grupo Traxion announced a successful issuance of MXN$2.0 billion in unsecured local bonds at a floating rate, structured in two tranches: MXN$1.0 billion due in six years at funding TIIE plus 195 bp and MXN$1.0 billion due in seven years at funding TIIE plus 200 bp. The bonds were issued under a CNBV-authorized program of up to MXN$10.0 billion, carry ratings of A+ (mex) from Fitch, AA from HR Ratings, and AA/M from Verum, and were listed on BIVA. The company will use proceeds to fund liability refinancing and will not alter its leverage ratios.

Fibra Inn’s room revenues declined 5.2% YoY to MXN$158.6 million in January, as a result of a 2.1 PP reduction in occupancy levels to 47.5%, partially offset by a 0.8% ADR increase to MXN$1,940. RevPar thus fell 3.4% to MXN$923.

Fibra Park Life (PLIFE26) will list its CBFI’s on March 17th on the BMV, aiming to raise approximately MXN$308 million. The Fibra will use proceeds to seed a four-property initial portfolio in Mexico City and Querétaro, totaling 287 apartments and 15,855 square meters of gross leasable area. The trust’s medium-term growth plan envisages expanding to at least 18 properties and more than 1,000 apartments over the next three years, requiring roughly MXN$3.0 billion in additional capital.

Fibra Shop secured a MXN$450 million sustainability-linked loan from BanCoppel to refinance existing liabilities. The three-year facility bears an interest rate of TIIE plus 220 basis points and will be added to the company’s existing revolving credit line with BBVA, increasing total available liquidity to MXN$1.6 billion to mitigate refinancing risk.

Gentera’s Peruvian subsidiary, Compartamos Banco Perú, successfully placed PEN74.7 million through a public issuance of negotiable certificates of deposit in the local debt market. The notes carry a one-year tenor, and a 4.34375% interest rate.

TV Azteca has entered a strategic partnership with PlaysOut, a global mini-games distribution platform, to integrate a games catalog into its mobile app. The initiative aims to enhance TV Azteca en Vivo’s entertainment offering with interactive experiences, with the PlaysOut content scheduled to launch in the first quarter of 2026.

Coca-Cola Femsa’s CEO Ian Craig will join the Board of Directors of Republic Services’, a US environmental services company. Mr. Craig’s appointment seeks to leverage his expertise in digital transformation and sustainability initiatives, according to Republic Services.

Fibra Terrafina obtained authorization to delist its CBFI’s from the Mexican Bolsa on February 18th.

OTRAS EMPRESAS

Pemex reported that total refined product output reached 908 thousand barrels per day, the highest on record, while crude processing averaged 1.27 million barrels per day, with high-value distillates rising by 119 thousand barrels per day. The company targets refinery output of 1.56 million barrels per day through investment, maintenance, modernization, and better residue utilization, while the variable refining margin averaged USD 12 per barrel and fuel sales rose nearly 8% from July to December, equivalent to 81 thousand barrels per day. In related news, Pemex successfully issued MXN$31.5 billion in the domestic debt market under a MXN$100 billion authorized program, which was the largest corporate debt issuance in history and marked Pemex’s return to domestic debt markets after six years. The issuance comprised MXN$9.0 billion in a 5.2-year floating-rate bond indexed to TIIE funding, MXN$17.0 billion in an 8.5-year bond priced at a spread over the MBonos 2034 yield, and MXN$5.5 billion in a 10.5-year bond linked to the interpolated Udibono 2035–2040 rate. The company will use proceeds to refinanced short term financial liabilities. All tranches received local-scale AAA ratings from S&P Global Ratings, Moody’s Local MX, and HR Ratings.

Kavak secured US$300 million in its Series F funding round led by venture capital firm Andreessen Horowitz, which contributed US$200 million through its a16z Growth fund. Other participants included WCM Investment Management, Lingotto Innovation, Foxhaven, Galdana Ventures, Stelac, and Allen & Company. No details were provided about the company’s updated valuation.

Mexican Fintech Plata has received a banking license from the CNBV, after a 3-year regulatory process.

Amazon Mexico announced a reduction in seller commissions for essential product categories such as food, health, and personal care, alongside a 51% average cut in Fulfillment by Amazon shipping fees for items priced below MXN$299, aiming to attract entrepreneurs and small businesses. The initiative allows sellers to improve margins and pass savings on to consumers, while new sellers will benefit from 12 months without a monthly fee and a low subscription cost thereafter if sales remain below MXN$26,000 per month.

TC Energy, a Canadian natural gas transportation infrastructure company, plans to invest up to CAD6 billion in 2026 in various initiatives including gas pipeline projects in Mexico (Villa de Reyes gas pipeline and Tula system, both with the CFE).

Solvento, a Mexican platform focused on liquidity and payment solutions for the logistics and transportation sector, secured a US$25 million financing backed by BBVA Spark. The funds will provide access to liquidity for transport operators and logistics companies.

ECONÓMICO

ANTAD’s same store sales increased by 2.0% YoY, with self-service up 2.9%, department stores down -0.2% and specialized retail rising 3.2%. Total sales grew 5.3% YoY, with self-service increasing 5.1%, department stores climbing 4.0% and specialized retail up 7.4%.

The Opportunistic Indicator of Private Consumption projects a 0.3% MoM and 4.5% YoY increase in private consumption in December 2025 and a 0.1% MoM and 4.4% YoY rise in January 2026, según el INEGI.

The Monthly Survey of the Manufacturing Industry anticipates a 0.1% MoM reduction and a 2.9% YoY increase in Manufacturing Production in December 2025, según el INEGI.

International visitors increased by 12.3% YoY in December 2025, INEGI reported. Total expenditure rose 1.9% YoY to US$3.77 billion while the average expense per visitor declined 9.3% YoY to US$372.3.

Afores’s AUM’s grew 26% YoY to MXN$8.5 trillion in January 2026, equivalent to 24% of GDP, according to Consar. This performance was led mainly by Profuturo (+26%), SURA (+24) and XXI Banorte (+22%). Investments included: government debt (51.9%), international equities (13.0%), private domestic debt (11.5%), structured (7.6%), domestic equities (7.2%), fibras (3.0%), commodities (1.6%), and other assets (+3.6%). Net gains amounted to MXN$158.5 billion in the period.

Foreign investment in the Mexican stock exchange peaked at US$195.7 billion in January, Banco de Mexico reported. Foreign inflows amounted to US$1.466 billion over the month.

Banco de Mexico’s released the minutes of its last monetary policy meeting. The Governing Board deemed it appropriate to pause the cycle of interest rate reductions. This was consistent with the assessment of the current inflationary outlook. It considered the adjustments to inflation forecasts and the need to continue evaluating the impact of the fiscal changes implemented at the beginning of the year, as well as FX behavior, the economic activity weakness, and the degree of monetary tightening that has been implemented.

Moody’s mentioned that Mexico’s credit outlook will depend primarily on the course of the USMCA and the fiscal strategy through 2027. The country’s 2025 fiscal results reflect slower-than-expected consolidation and a weaker growth environment. Government support to Pemex will continue to be necessary given operating losses and negative cash flow.

Mexico and Canada began this week the development of a bilateral action plan that will be presented in the second half of the year, with a view to strengthening economic integration ahead of the review of the USMCA, stated Economy Secretary Marcelo Ebrard.

President Claudia Sheinbaum will present a reform initiative to cut pensions of high-level public employees to no more than 50% of the President’s salary. She expects to save MXN$5 billion with such a measure.

Subasta CETES: 28-day CETES -4 bps to 6.84%; 91-day CETES -5 bps to 6.95%; 182-day CETES +1 bps to 7.11% and 364-day CETES -15 bps to 7.22.

Descargar PDF: Mexican Market Chatter February 12th – February 19th